FactorMiner – Your First Step Toward Smarter Factor Discovery

Portfolio123’s new FactorMiner is now available – and it changes how you start building quantitative strategies —>

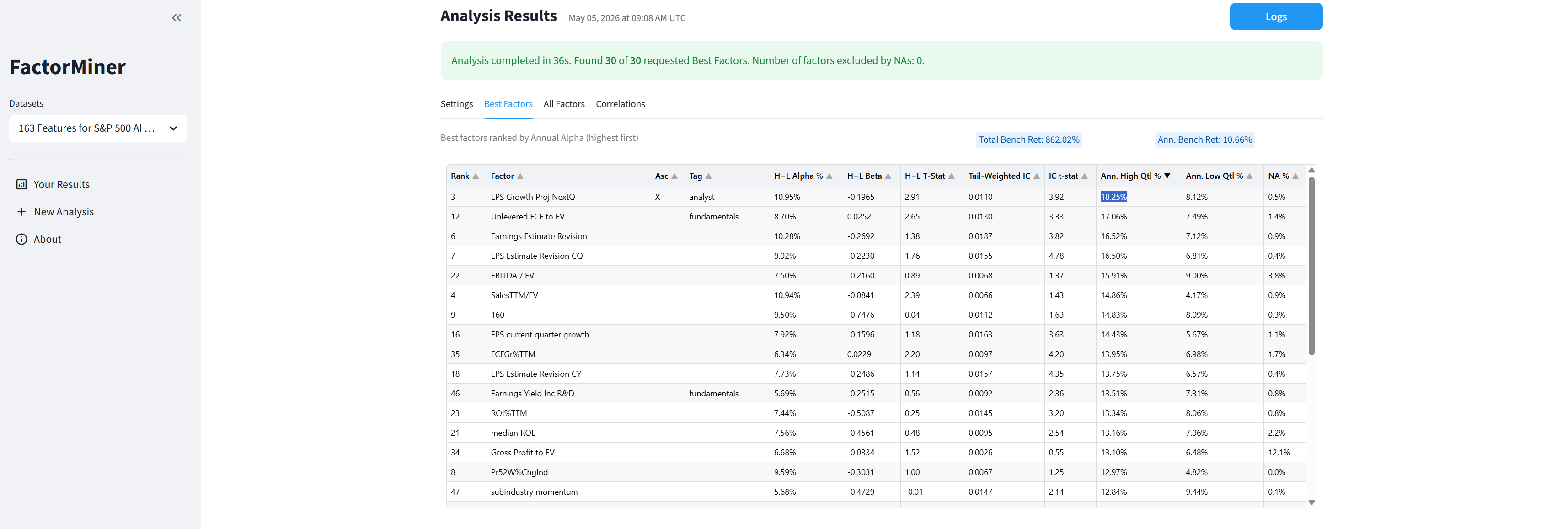

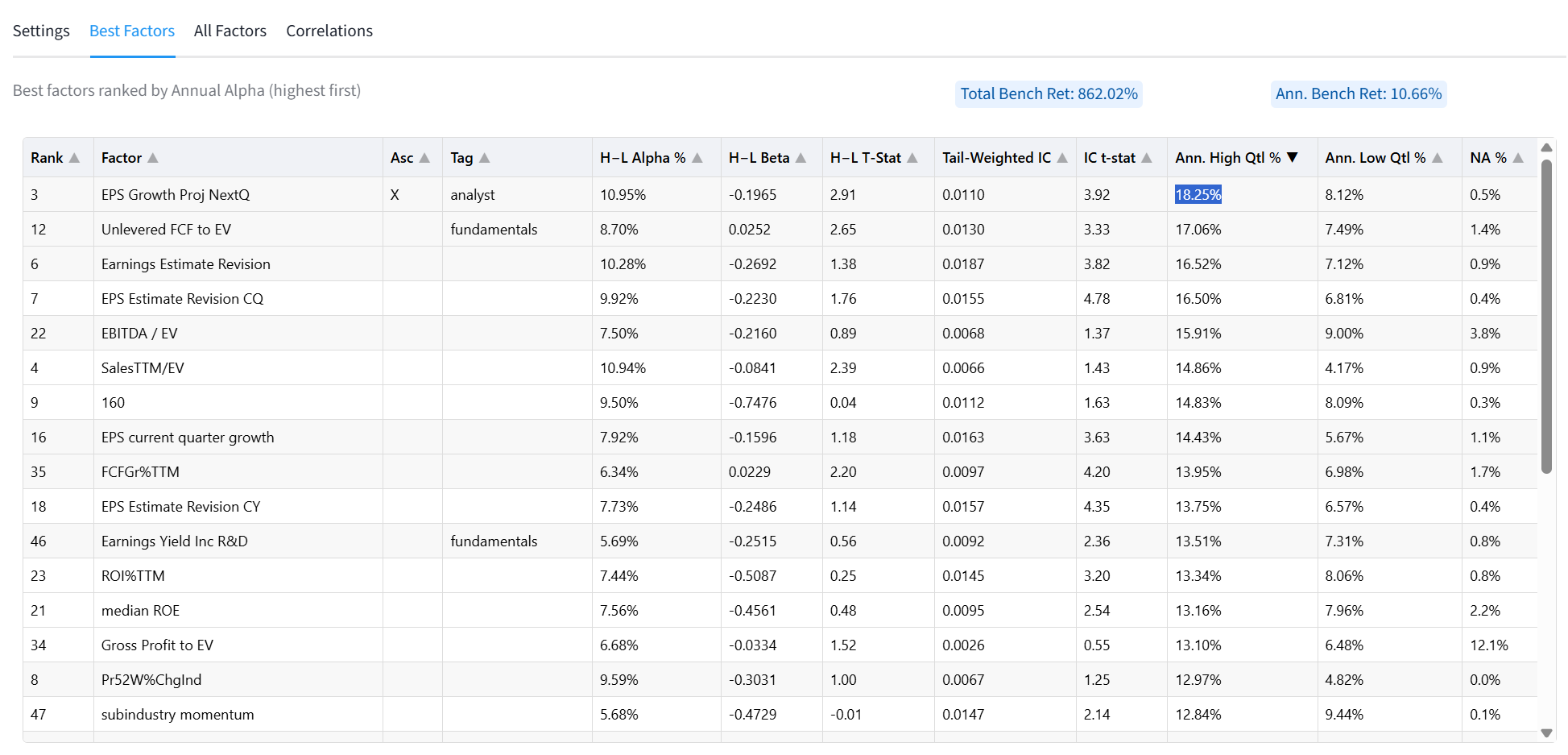

What FactorMiner Does

FactorMiner evaluates each factor independently and reports key metrics:

Annualized alpha, beta, tail-weighted IC, t-statistics

High/low quantile returns

Missing-value coverage

Factor correlations

It can rank factors by Alpha or IC, automatically detect the best sort direction for long/short, and create a subset of the best factors using a maximum correlation coefficient.

How to access it:

Go to RESEARCH → TOOLS → Download Factors

Create a Factor List with your superset of factors

Generate the dataset (requires API credits)

Click Analyze → FactorMiner Launch

Review settings and click analyze

Note: FactorMiner currently lives inside “Factor List” but will soon move to a new home with other “apps”.

Why FactorMiner Matters

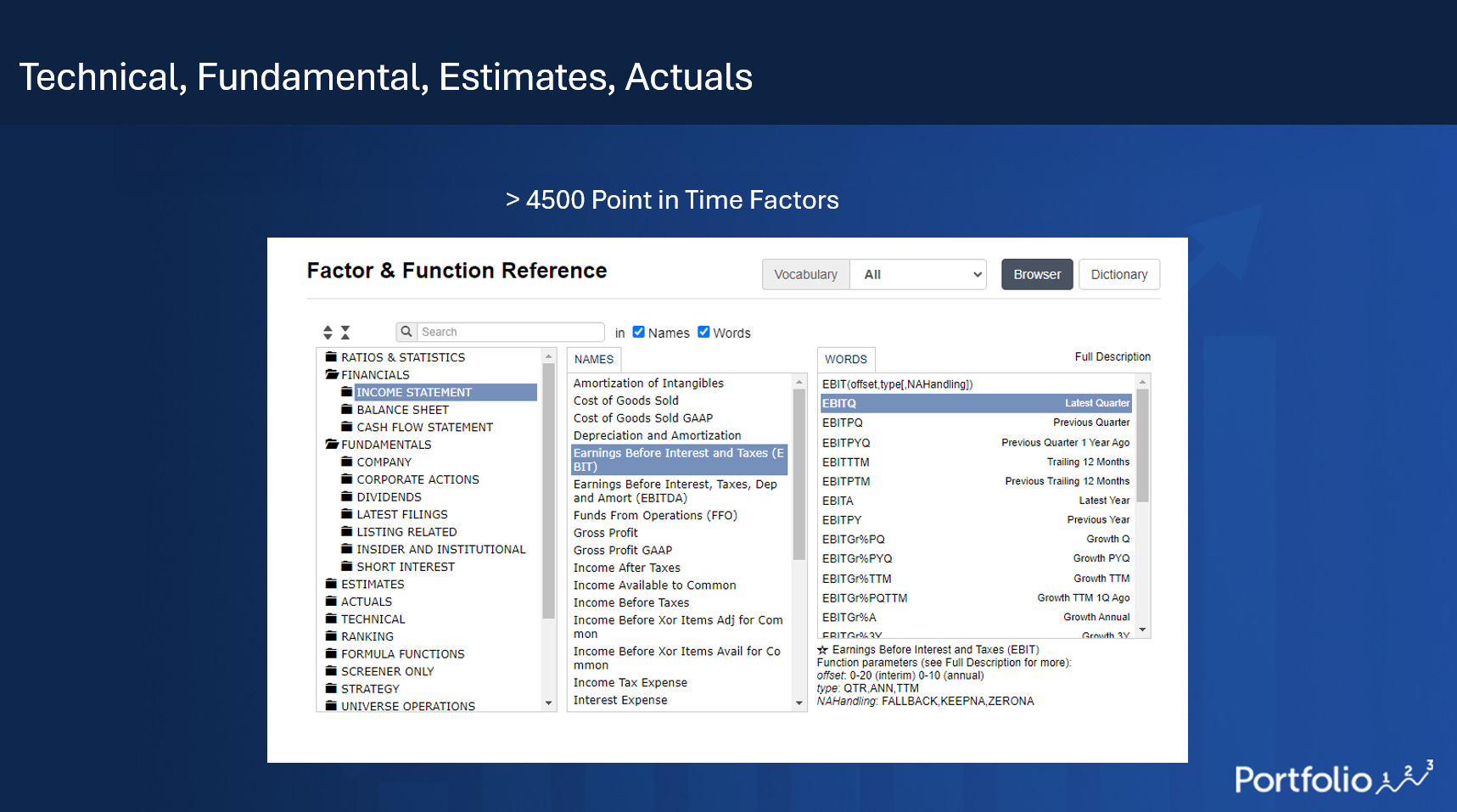

Factor libraries can be large!

A single idea – value, quality, growth, sentiment, revisions, momentum, or risk – can have dozens of formula variations.

FactorMiner turns that problem into a repeatable workflow:

Which formula variation has the strongest standalone predictive power?

Should higher or lower values be preferred?

Does the factor work in the top tail, bottom tail, or long/short spread?

Is the factor too sparse because of missing data?

Is it redundant with other selected factors?

For long‑only investors, the one stat to watch is:

Ann. High Qtl % – the annualized return of the top bucket.

That’s your starting point. Simple & Data‑driven!

What Users Are Saying

“I just was able for the first time since several months to substantially improve my US strategy... Thanks to FactorMiner”

“20 year simulation based on ML validations: Sim CAGR before 46% → Sim CAGR now 61% at same turnover...”

“Would never have thought that there is THAT much juice left to squeeze in simple univariate feature engineering.”

“Anyway... I love it so far.”

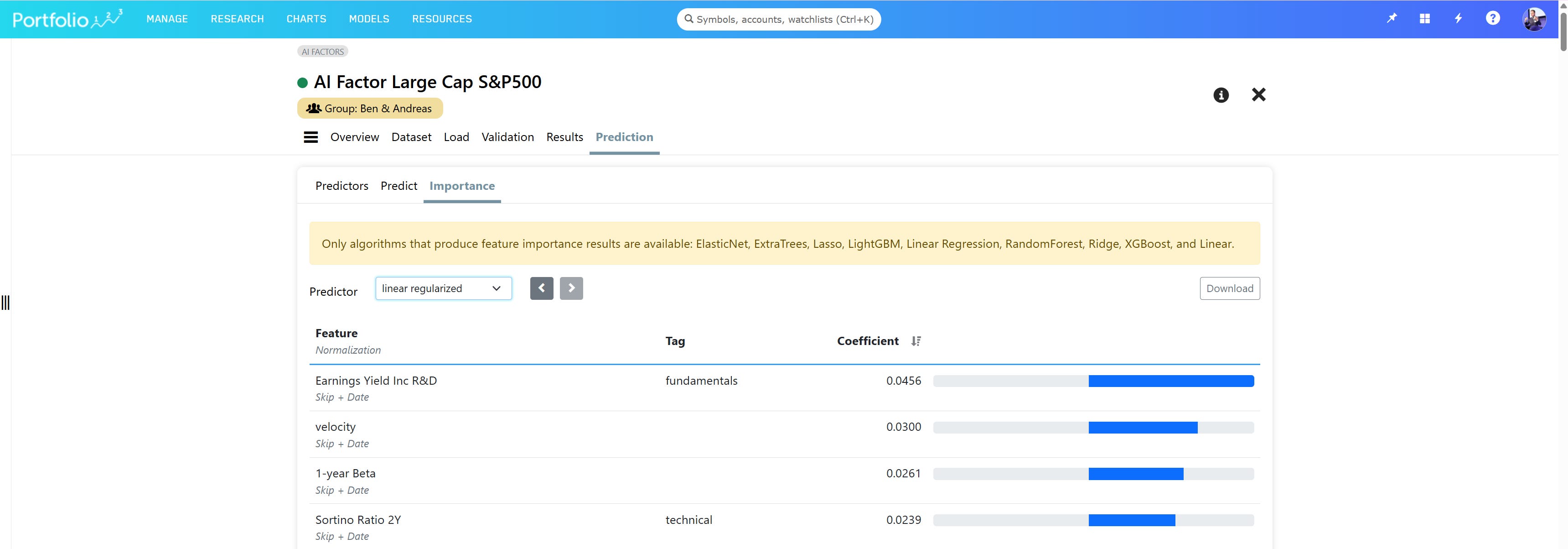

🚀 The Natural Next Step: AI Factor via Linear Machine Learning

FactorMiner is a strong pre-processing tool for AI workflows. It helps you:

Quickly generate candidate features

Factors with stronger alpha

Filter out factors with excessive missing data

But once FactorMiner has pointed you toward promising signals, you’re ready to move from univariate to multivariate.

That’s where AI Factor Linear (ElasticNet I + II) comes in.

Instead of looking at one factor at a time, AI Factor Linear evaluates all factors together – automatically handling correlation and weighting them for maximum predictive power.

I love both methods to get my head around the data!

FactorMiner for single-factor intuition – this is important: always good to know what gives the biggest edge!

AI Factor (for example via linear regularized MLs) for multivariate interaction power.

Together, they give me the full picture!

Best regards,

Andreas

P.S. —>

Zoom Call Link: https://calendly.com/portfolio123meeting

Trial Link: https://invest.portfolio123.com/get-started/

Link to the Portfolio123.com Community: https://community.portfolio123.com/t/factorminer-is-live-faster-factor-discovery-for-alpha-research-and-ai-feature-engineering/76504