Financial Repression: Ways to invest...

...or be run over by inflation!

I get a lot of feedback from investors and the biggest problem for them is: time!

I just talked to a CEO of a small cap company, he is putting in 60+ hours a week, at the same time he is out of the market and missed the whole bull market since the end of 2022. Now regrets are high, and fear is also (is this the top?).

Look, I been there, if you work 60+ hours, provide for kids, parents get sick, the best friend dies of a heart attack: I was (and still am a bit) in this situation. Nothing to look down on!

If you are putting in 60+ hours, you do not have the time to be the next breakout trader realizing 50%+ years.

And you do not have the time to research the small cap value momentum edge and realizing 30%+ years.

Be honest and be realistic.

At the same time, if you are not investing in quality stocks, quality real estate, gold and (maybe) a bit of bitcoin as a diversifier you are going to be run over by inflation.

The US runs 6% deficits (let’s see what Musk and Trump are going to do about it, fixing this could happening, but I think we must wait for results), which means in the midterm inflation is coming back (and even now it is here!).

This (financial repression) is a bit worse now (not as bad as in the 1940s), but this (financial repression) is always the case: if you are not invested in hard assets, inflation is going to (at least) pressure you. So, working hard is not going to cut it. The combination that cuts it is: work hard + think 1h about money once a week!

Have a look at upper class families (mostly aristocrats, their investing is grained in their culture) that are around over 1000 years (yes, such families exist).

What do they own? Fertile Land (hard asset), Gold (hard asset), Quality Stocks (hard asset), Quality Real Estate (hard asset).

They do not invest in anything close to paper money (Bonds, money market funds) strategically. And they do not care about volatility because it does not matter if you own 2 billion, then 1 billion and then 3 billion 20 years later. Volatility is the problem of the middle class: this is the nut we need to crack.

So, what to do?

I am not an expert in real estate, so I am not writing about it (though I own it, 50% of my money is in real estate, we got pure lucky and bought in 2008 and 2011, both estates are up > 75% and we locked in 2% interest rate until 2030) so search for other sources.

So how to invest outside of real estate, if you have almost no time whatsoever?

First Step: Stop listening to fear mongers!

Here is a blog post on #secularBullMarketUSA (first post on Twitter was at the end of 2018, I am the only one using it :-)).

Huge Secular Bull Market: What most macro models get wrong! #SecularBullmarketUSA

Let us start with the most important factor (if other factors are in play, later!): Demographics:

Second Step: combine different edges

Which edges exist in the market that fit investors THAT COME BACK FAST after a market crash. Only those edges do so (nope, pure high beta does not, careful!):

Low Volatility Quality (Buffett stuff and Expecting Dividend stuff)

Quality Growth (think Coca Cola in the 90s and Amazon today)

Small cap value quality momentum (also comes back fast after a crash) is a great diversifier too, but it is not really a good fit for people with no time: Those models are hard to research and if you rent them the good ones are expensive. + you need to trade around a monster big bid-ask spread which costs time too.

Here is one (!) solution: I took out of sample strategies from Portfolio123 and build the following book (all the strategies are free with a subscription of P123, no extra cost).

Here is a video on how to do so:

For Investors: How to build a Strategy Book with Time Tested P123 Portfolio Strategies

Here is the link to the strategy book https://www.portfolio123.com/port_summary.jsp?portid=1812900

But: This is only a base model. The aim of the model is to beat the SPY while printing the same risk as the SPY. So, are you fine with 50% drawdowns? Be honest to yourself or sell in panic when the market and your model prints a 50% drawdown.

If you are young the solution could be to cost average into a model like this, if you are 5 years before you want to retire, or have a big junk of money to invest right now change the risk profile of the model (or cost average in the riskier version).

Add hedges or diversifiers (like short term Bonds with no duration risk: BIL) to the model and find out what risk profile fits to you. If you like Bitcoin, add a 5% weight to it, etc.

Same model with a 11% TWM (2 times short on IWM) position:

Now even that model will have a ton of stocks to be managed every week (some models in the book rebalance weekly).

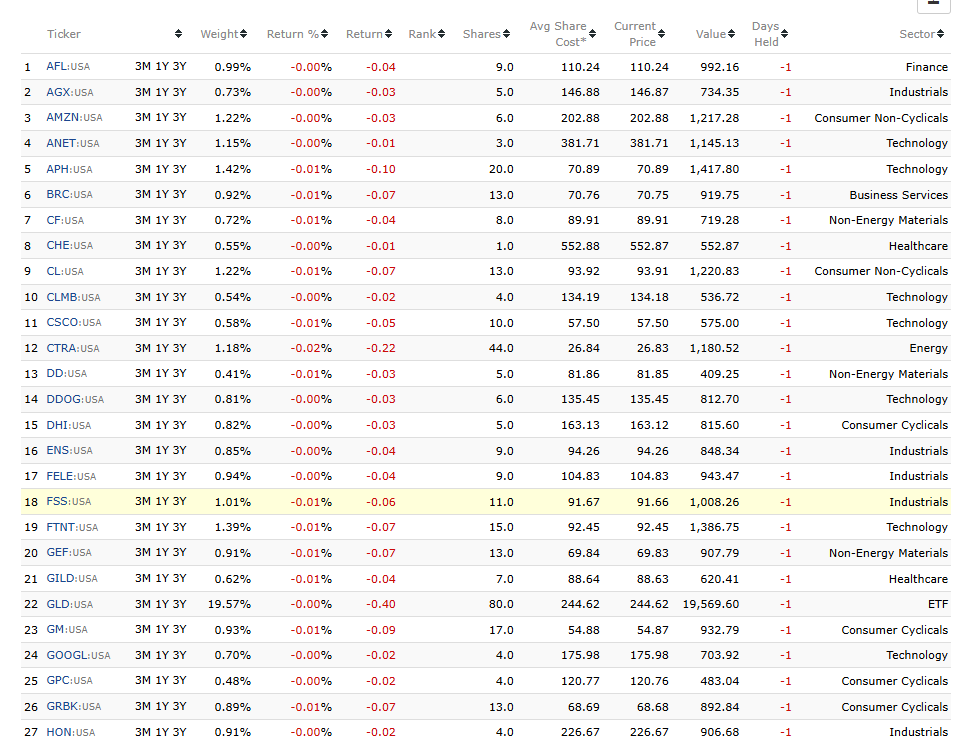

I just show the first 27 Stocks here (altogether we are talking about 71!)

For party kitchen discussions: yes, the model owns NVDA.

Now I get the following feedback: that is a lot of work too!

Well, now you hurt my feelings, over 20 years of research is in that strategy book ;-)

So, if you do not want to do that, outsource it:

Find a financial advisor, show this (or another) portfolio book, sign all the risk papers and ask them to implement it for you (yes, it will cost you 1.25% - X a year, no free lunch).

If that is not the solution for you and you are young(er)…

…cost average into the SP500 via the SPY 0.00%↑ . The SP500 is one of the best trading systems in the world and with big money (> 10 billion of AUM or so) it is extremely hard to beat.

If you have a big chunk of money, split it up (24-36 months splits might be fine) and cost average that too.

Why is the SP500 a good trading system and not an “index”? The SP500 combines momentum (+ fundamental momentum) + Quality. Very, very, very smart people run that “system”. Plus, you have the #secularbullmarketUSA as your tailwind.

To be blunt, forget the rest of the world, the US is the place to be, China is not investable (forget it, just forget it and now forget it), and Europe is dead in the water (demographics) and emerging markets are at the peril of the dollar.

All the best and best regards.

Andreas

____________________________________________

The information on from Andreas Himmelreich / QuantStrike and this video / blog is for information and discussion purposes only. It does not constitute a recommendation to purchase or sell any financial instruments or other products. Investment decisions should not be made with this video, and one should consider the investment objectives or financial situation of any person or institution.

Investors should obtain advice based on their own individual circumstances from their own tax, financial, legal and other advisers about the risks and merits of any transaction before making an investment decision, and only make such decisions based on the investor’s own objectives, experience, and resources.

The information from Andreas Himmelreich / QuantStrike and this video / blog is based on generally available and paid information and, although obtained from sources believed to be reliable, its accuracy and completeness cannot be assured, and such information may be incomplete or condensed. All performance results are hypothetical and the result of back testing only. Out-of-sample performance may be different. No claim is made about future performance.

Investments in financial instruments or other products carry significant risk, including the possible total loss of the principal amount invested. Andreas Himmelreich / QuantStrike and this video / Blog do not purport to identify all the risks or material considerations which may be associated with entering any transaction. Andreas Himmelreich / QuantStrike and this video / blog accepts no liability for any loss (whether direct, indirect or consequential) that may arise from any use of the information contained in or derived from Andreas Himmelreich / QuantStrike and this video / blog.