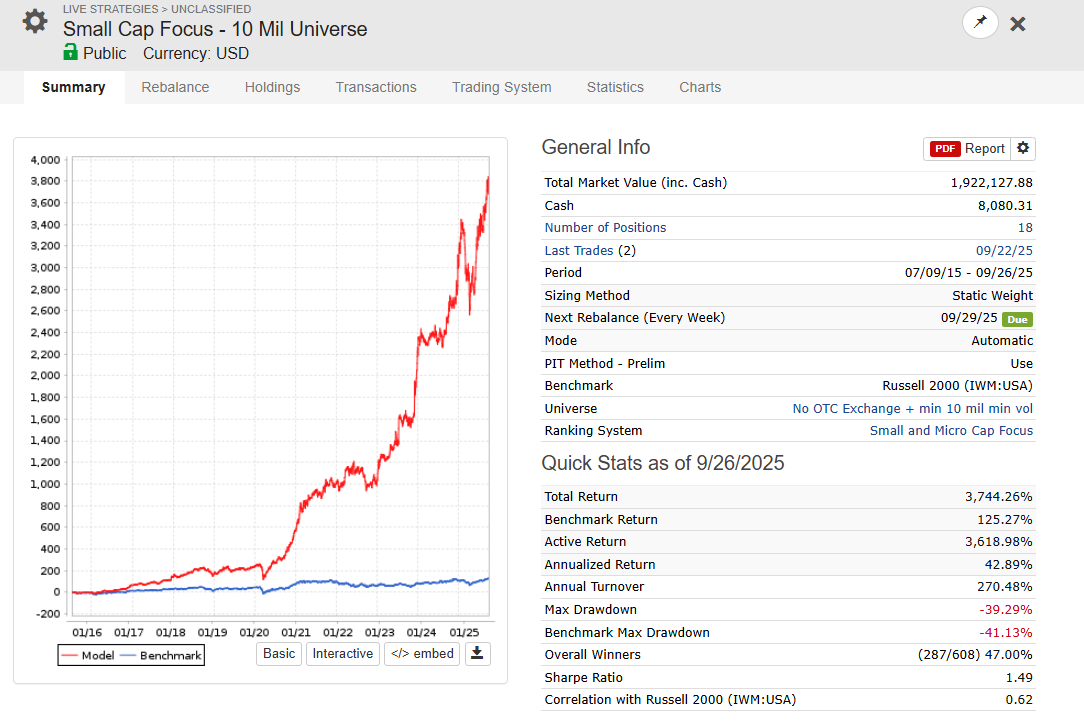

I. Free Systematic Strategy of the Week 🚀

https://www.portfolio123.com/port_summary.jsp?portid=1866851

Robust Design:

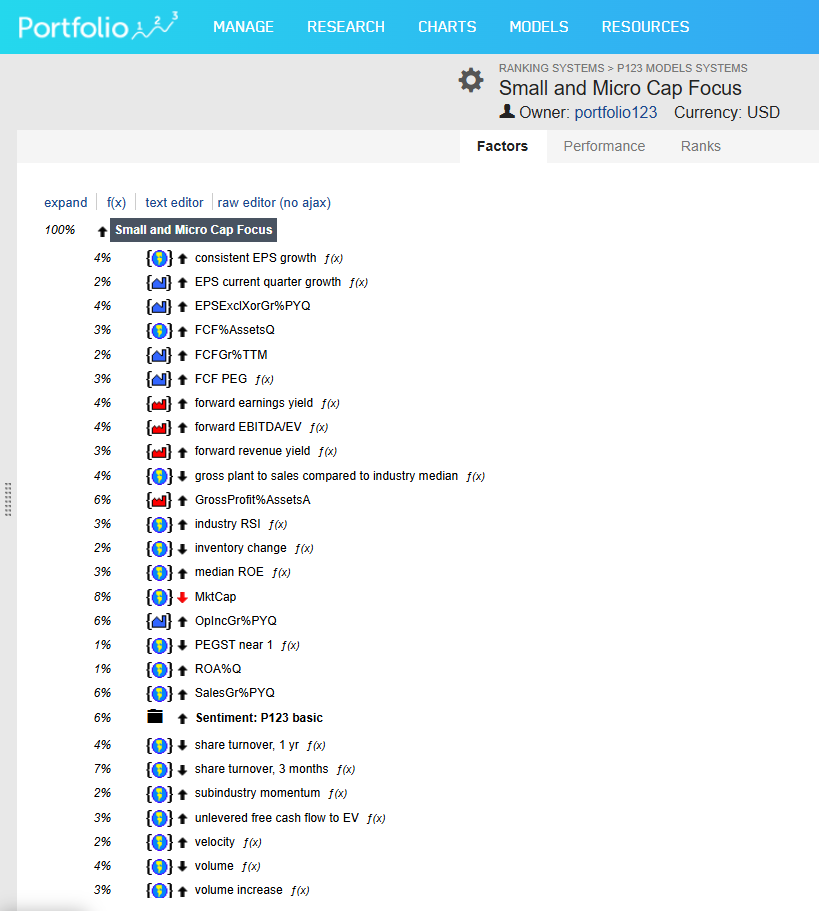

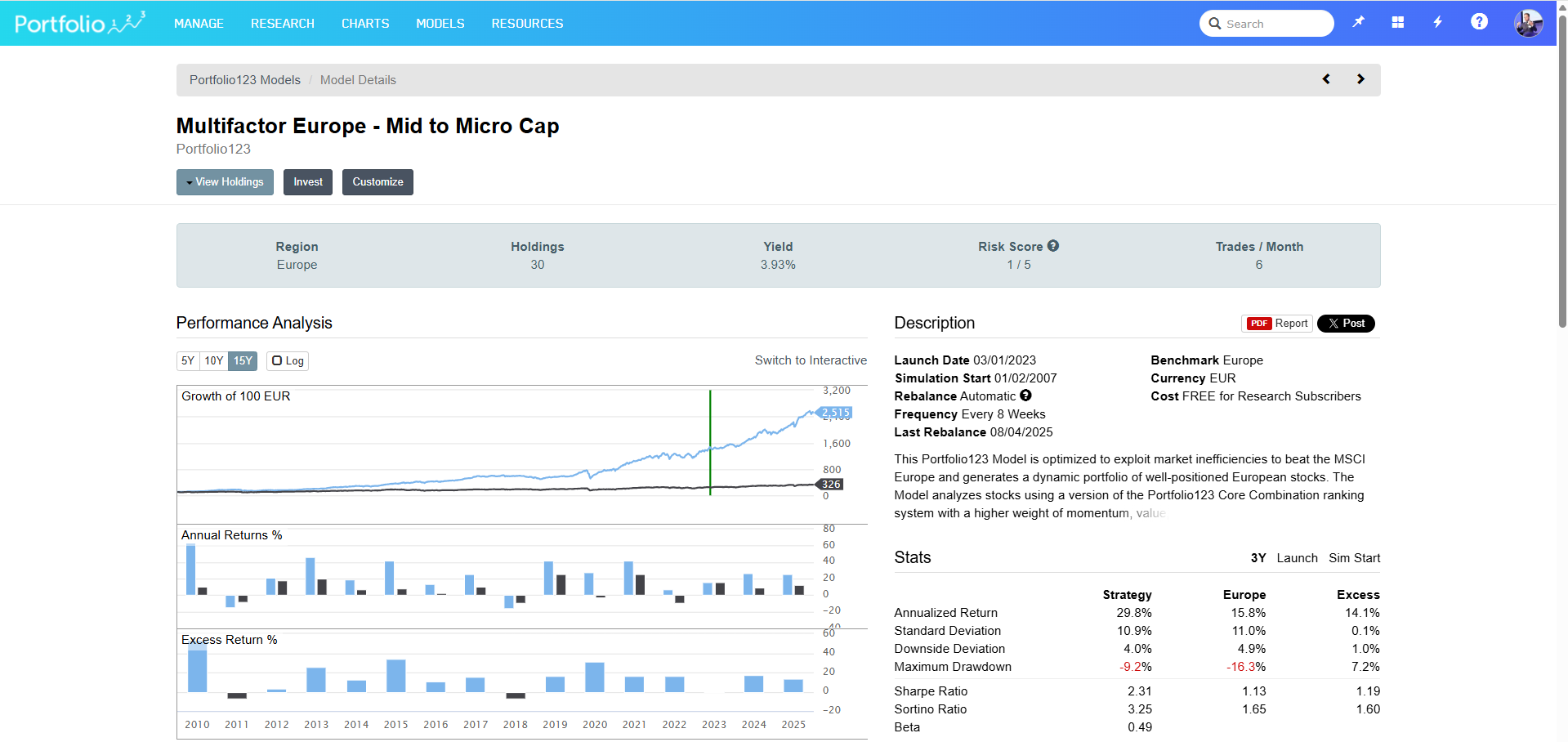

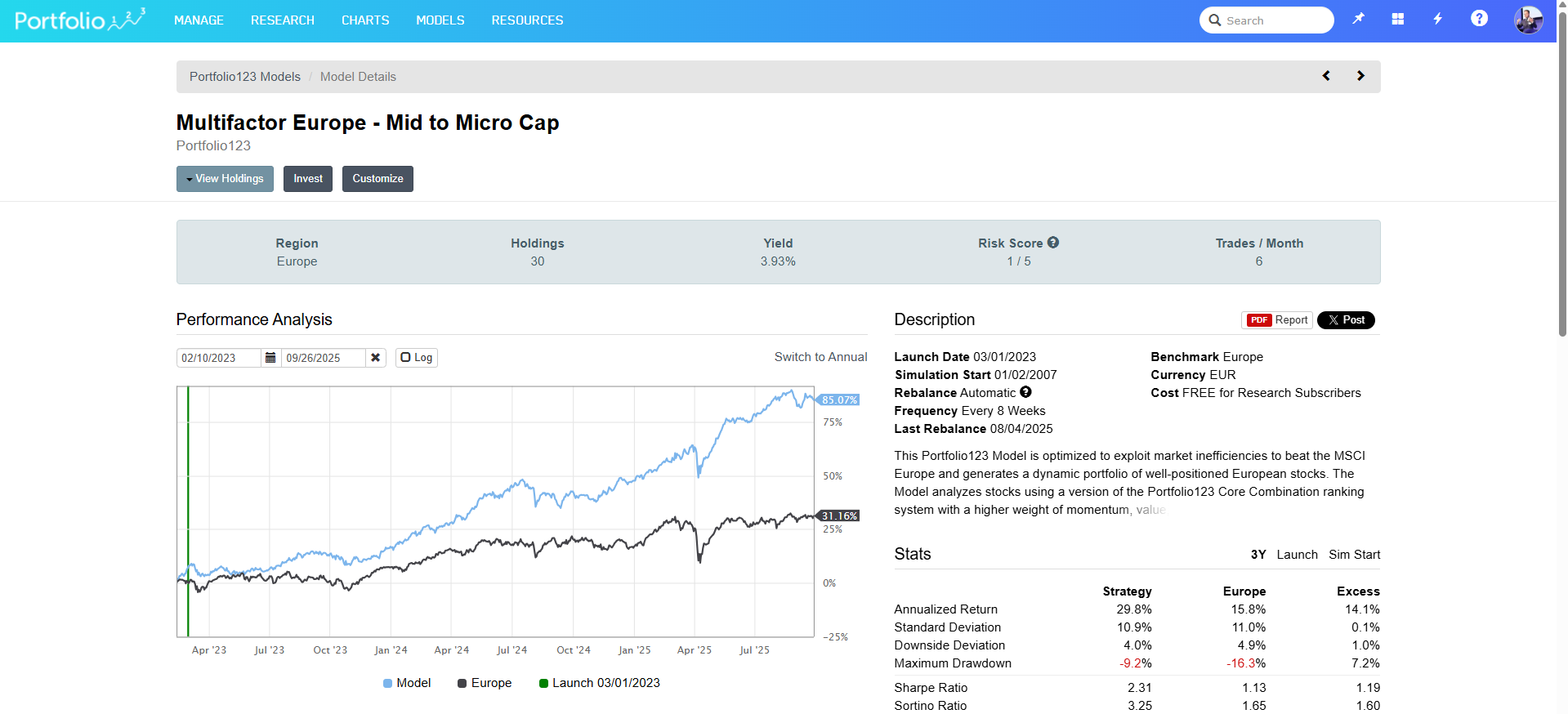

Ranking System:

https://www.portfolio123.com/app/ranking-system/403577

Small and Micro Cap Focus

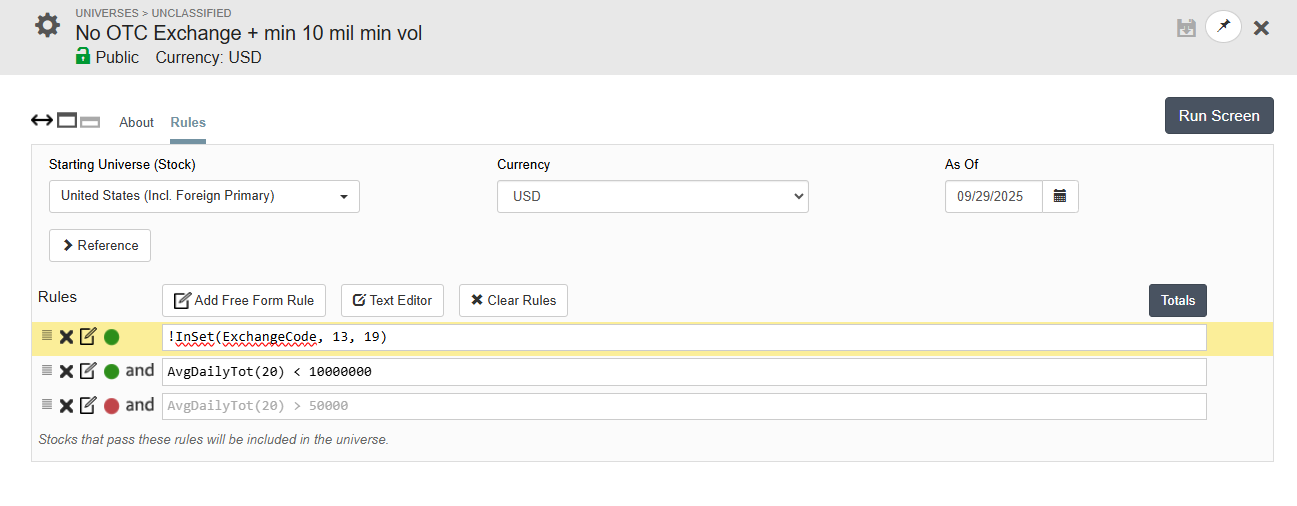

Small Cap Universe

Auto Trade

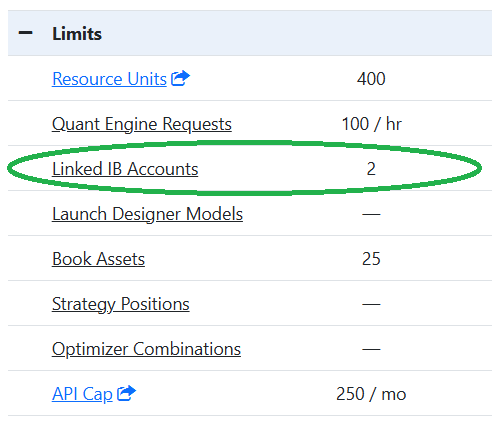

For a 25$ ($35 Monthly) Screener Subscription https://www.portfolio123.com/sv/register/retail you can auto trade (for example!) the above Strategy via a P123 Trade Account and a connection to Interactive Brokers (pro Account needed!) or Tradier:

Screener Subscription (excerpt!):

Video on how to autotrade:

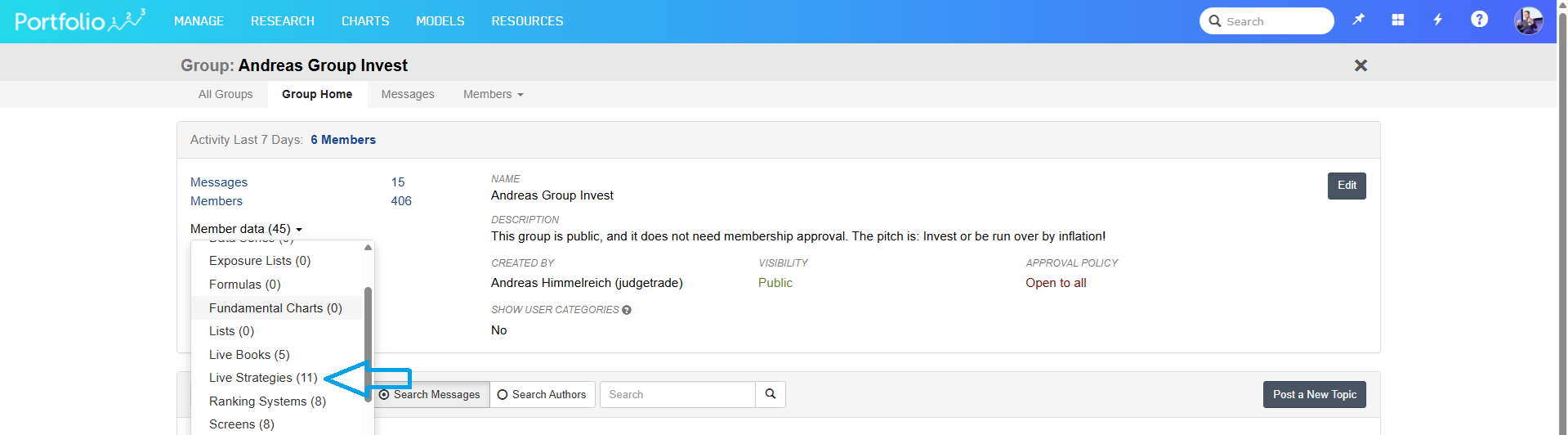

Strategy Books are now shareable in Research Groups of Portfolio123.com

We are just starting out, but I will share a ton of Strategy Books in the coming weeks: Perfect for private Investors that want to use time proven out of sample Strategies in one holistic Strategy Book!

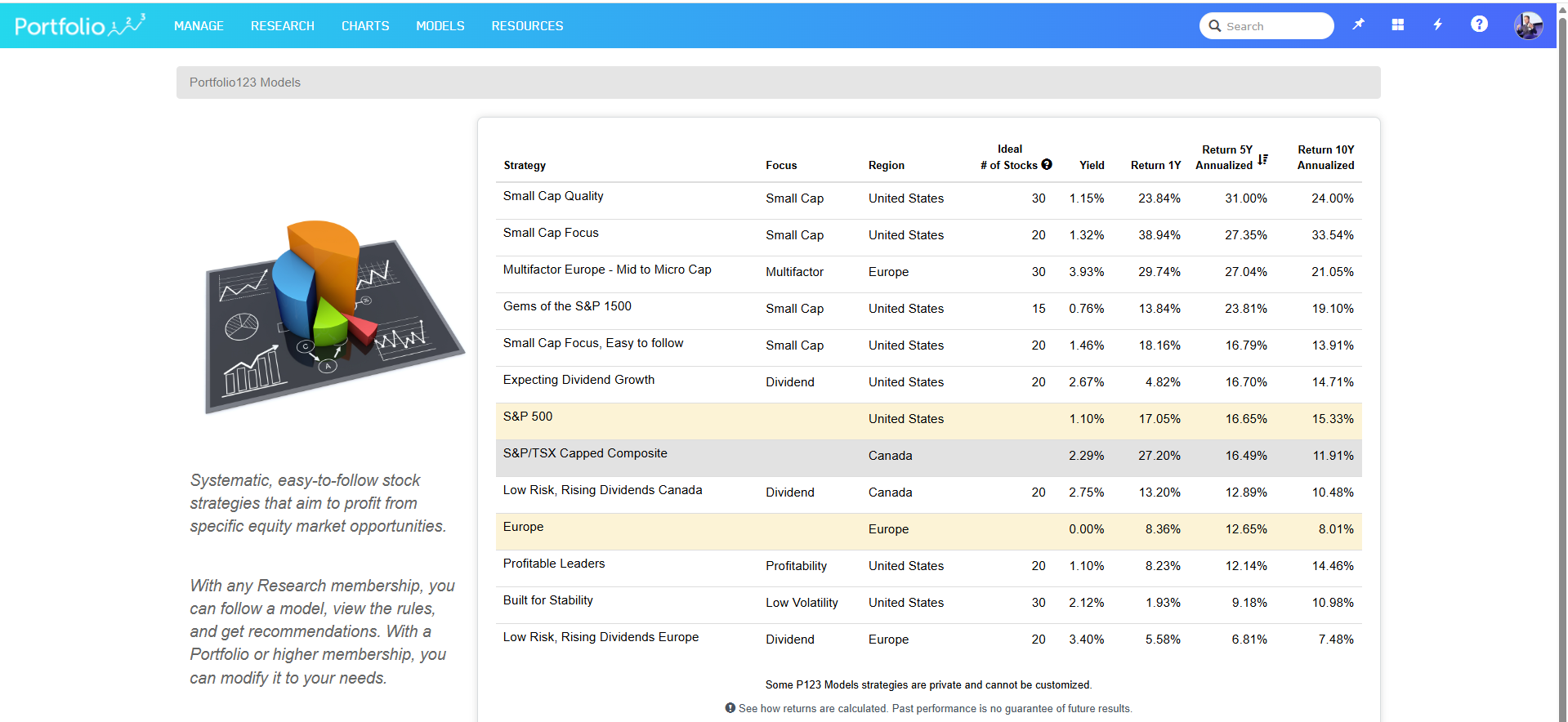

More Strategies are here —> Models —> Portfolio123 Models

https://www.portfolio123.com/app/investment/add-new?browse=1

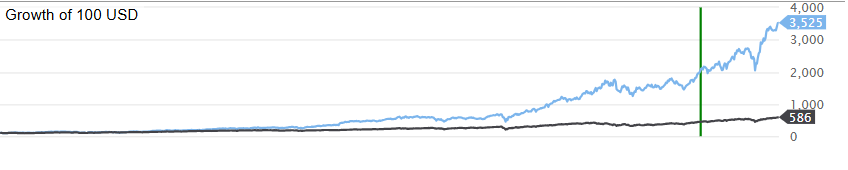

My favorite free Portfolio123 Model:

https://www.portfolio123.com/app/investment/add-new?browse=1&t=STOCK_STRATEGY&pid=1711518

Out of Sample Live Trading of the above model:

II. Rebalance 💡

Wait until the rebalance is through about 1-2 hours before the market opens on Monday!

More free Strategies are in my Research Group with now 406 subscribers here:

https://www.portfolio123.com/app/group/317

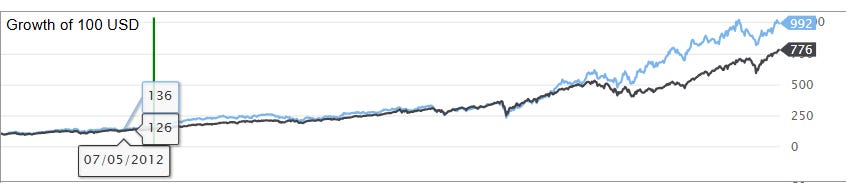

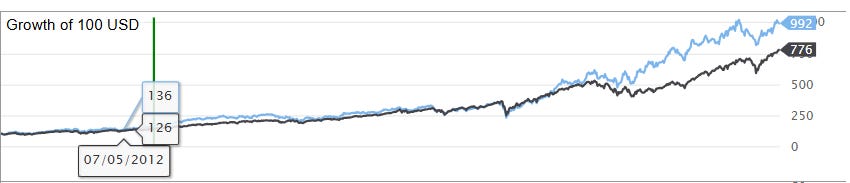

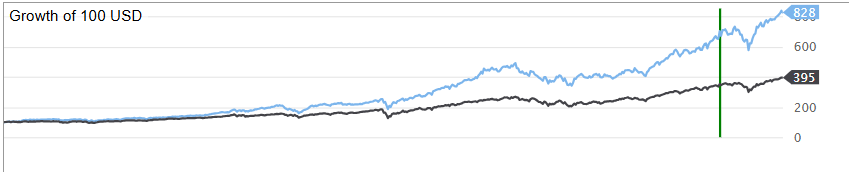

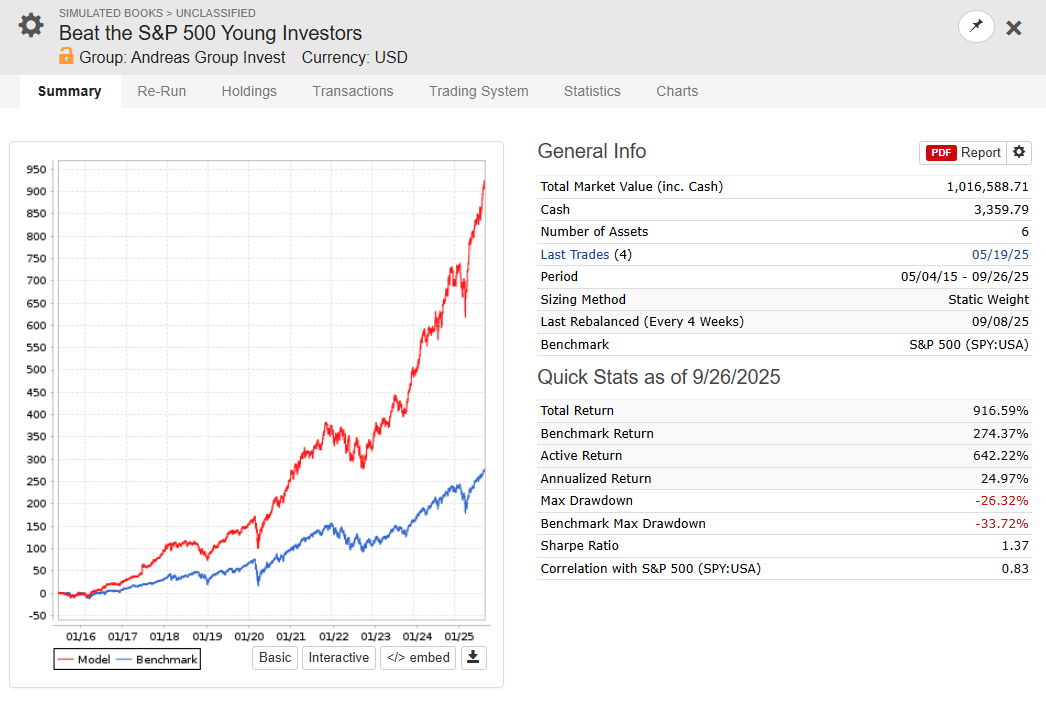

Strategy Book Beat the S&P 500 Young Investors: Out of sample live trading since October 2024

https://www.portfolio123.com/port_summary.jsp?portid=1854360

This is a strategy book (a portfolio of ETFs and Live Strategies) with the following positions:

Gold 25%

Bitcoin 5%

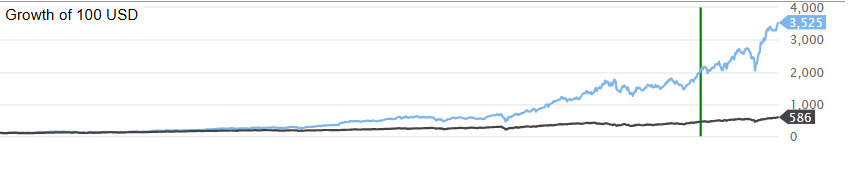

Buffett (A Live Portfolio Strategy with an Out of Sample History (Live Trading) since 2013! https://www.portfolio123.com/app/r2g/summary?id=1039193 —> 25%

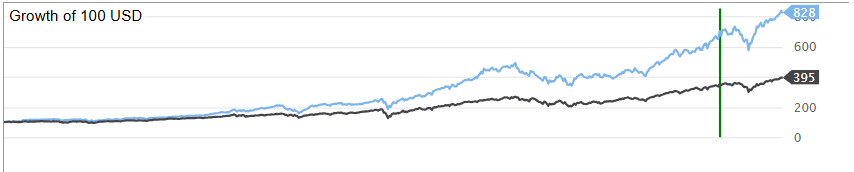

NASDAQ 100 best growth stocks max. 10 Stocks, Free! https://www.portfolio123.com/app/r2g/summary?id=1757039 —> 15%

Higher Beta + Earnings in Top 10% S&P500 Universe, Free!

https://www.portfolio123.com/app/r2g/summary?id=1765750 —> 15%

Russel 3000 Profitable Growth Stocks Free!

https://www.portfolio123.com/port_summary.jsp?portid=1812296 —> 15%

Here is the Strategy Book:

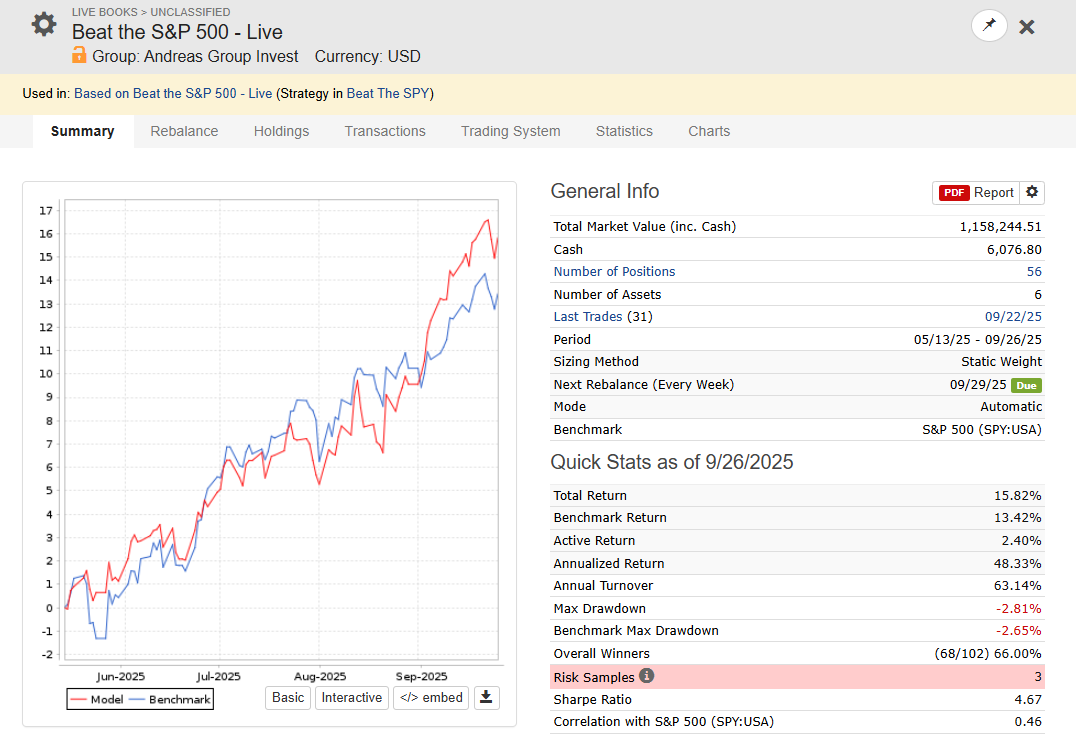

Corresponding Live Book

Remember, you can auto trade the Live Books (and the Live Strategies).

https://www.portfolio123.com/port_summary.jsp?portid=1854362

Why a Strategy Book?

Because it naturally captures cross-factor mean reversion. It automatically sells into areas of strength (e.g., today Gold and Growth) and reallocates into areas of weakness (e.g., Quality and Bitcoin). This implicit timing effect is extremely difficult to replicate with explicit factor timing. Remember: no factor works all the time. Even Buffett underperformed from 1996–2000, only to shine when Growth collapsed after 2000.

III. Cross Factor Mean Reversion 📊

Why is cross-factor mean reversion so powerful?

First, mean reversion has persistence. When a factor gets extremely out of favor, it often rebounds with force. This is especially true for classic factors like value or low volatility. They can go from being the “worst idea ever” to “everyone’s favorite allocation” in just a few months.

Second, it capitalizes on behavioral overreaction. Markets tend to over-discount factors. If investors flee value stocks en masse, the price distortions become extreme. Eventually, rebalancing flows and fundamental corrections bring those factors back into favor.

Third, factors are usually uncorrelated at turning points. When growth cracks, value might shine. When high beta stumbles, low volatility leads. That low correlation between factors—especially during reversals—makes timing even more lucrative, if done right.

Factor timing is incredibly noisy. Trying to predict which factor will outperform next is one of the hardest problems in quantitative investing. Macro signals, interest rates, and valuation spreads help, but they’re imprecise and often lag. It’s easy to chase strength too late or exit weakness just before it rebounds.

False starts and whipsaws are common. You might see value outperform for a few weeks, only to give it all back. Factor rotations aren’t smooth—they’re violent and often disrupted by market shocks like Fed actions or geopolitical events.

Cross-factor regimes also don’t always follow macro logic. Sometimes low volatility leads in bull markets. Sometimes momentum fails during panics. These reversals behave more like investor crowd psychology than economic textbook patterns.

Timing also requires Goldilocks speed - neither too fast nor too slow. If you’re too slow, you miss the bounce. If you’re too fast, you churn capital reacting to noise. Cross-factor moves often happen in bursts, so even a few days later can cost the edge.

Why combining strategies with clear factor tilts with regular rebalance wins?

Because timing is so difficult, many smart strategies simply hold a balanced exposure to multiple meta-factors, let mean reversion work in the background, and regular rebalance.

For example, building a book of single-factor strategies—like one value, one momentum, one quality—and letting them rotate inside the book is a form of implicit timing without having to make explicit calls.

The takeaway

Cross-factor mean reversion is one of the most durable and powerful forces in quant investing. It captures the natural ebb and flow of entire factor styles rotating in and out of favor. But trying to time those shifts is incredibly hard due to noise, false starts, and behavioral volatility. The better approach is often diversified exposure across factors and allowing the reversion to work for you—not against you.

Cross-factor mean reversion + 25% gold = hidden alpha combo?

If you’ve built a diversified book of multi-factor equity strategies—especially ones that benefit from cross-factor mean reversion—you might already have something robust. But adding a 25% gold position can take it to another level.

Why gold adds so much value

First, gold is non-correlated to equities. It doesn’t care about earnings revisions, factor momentum, or what the Fed says about buybacks. It often moves in a different direction than equity factors - making it an ideal diversifier.

Second, it acts as a tail risk hedge. In moments of market stress, inflation shocks, or geopolitical risk, gold can spike while equities suffer. That buffers drawdowns and creates dry powder for rebalancing.

Third, it improves Sharpe ratio and reduces volatility. In both backtests and real usage, a 20% gold allocation has often produced smoother equity curves, lower portfolio volatility, and better risk-adjusted returns.

Fourth, it’s a great fit for cross-factor regime shifts. When one equity factor crashes and another hasn’t picked up yet, gold provides a bridge—helping your portfolio hold ground until the next leader emerges.

Gold and cross-factor timing

Think of gold as the shock absorber in your equity factor engine. It’s the rotational glue that helps you survive messy handoffs between winners and losers. It’s the anchor when nothing else in equities works.

All right, have a great week!

All the best and best regards.

Andreas