Investing Strategies

This post is about how to use time proven strategies from Portfolio123.com and design your own Portfolio of Strategies (Strategy Book as we call it).

Here we go: Strategies from P123 and from P123 Members I like:

Buffett

https://www.portfolio123.com/app/r2g/summary?id=1039193

Strategy from Marc Gerstein (very good Quant, used to work for P123).

It is out of sample since the green line (end of 2013). The blue line is the strategy, the black line is the benchmark. The descriptions of the strategies come from the designer of the model.

This is a model inspired by the philosophy of Warren Buffett. While much of what he actually does is based on his personal skill and judgment and cannot be replicated in a model, we can and have built a model that is guided by three important ideas that characterize his approach: fair valuation, solid company fundamentals and reasonable consistency. The portfolio holds approximately 20 stocks and is rebalanced every four weeks. To be eligible for consideration, stocks must pass these conditions:

Pass liquidity tests

Market cap between of at least $250M

Industry does not exceed 25% of total

Not be in an industry whose financial characteristics we deem incompatible with fundamental screening and ranking

Meet various tests relating to financial strength, return on capital and consistency of performance.

The top ranked stocks are picked using a ranking system based on valuation, growth and earnings quality.

P123 Value and Momentum

https://www.portfolio123.com/app/r2g/summary?id=1132342

Value Momentum from Marco (Founder of P123).

You can see the strategy for this free P123 model here. This strategy finds value plays with prices moving upwards with a MidCap concentration. It holds approximately 30 stocks, has a relatively low yearly turnover of less than 150%, and is liquid for amounts of $1M and more. The top ranked stocks are picked based on a ranking system that combines value factors and momentum factors. The value factors make up 60% of the rank and the momentum factors 40%. The highest-ranking stocks must also pass these conditions:

Have increasing ROE in the past 12 months

Pass liquidity tests

Market cap of at least $500M

Sector does not exceed 25% of total

No MLP's to avoid K-1's at tax time

If a stock's rank drops below a certain threshold it is replaced by a higher ranked stock. This strategy was originally proposed by two Portfolio123 members: Denny Halwes and Gordon Tan.

P123 Expecting Dividend Growth

https://www.portfolio123.com/app/investment/add-new?browse=1&t=STOCK_STRATEGY&pid=1503605

This Portfolio123 Model seeks stocks with high and growing dividends, with reasonable risk compared to the market. The Model picks only stocks that increased their dividend in the last year. In contrast, in assessing prospects for dividend growth, the Model focuses not just on historical payout trends but also on analysts and market assessment of growth prospects (with a particular focus on recent revisions). Finally, the stocks picked must pass a quality screen, and the underlying portfolio needs to be reasonably diversified by sector.

SlingCharts: S&P 500 Dividend Income

https://www.portfolio123.com/app/r2g/summary?id=1420190

Strategy from Walter; very good Quant and long, long time P123 Member.

Higher Beta + Earnings in Top 10% S&P500 Universe, Free!

https://www.portfolio123.com/app/r2g/summary?id=1765750

From me, careful, only 10 Stocks and higher Beta!

Small Caps 25 from Easy to Trade US

https://www.portfolio123.com/app/r2g/summary?id=1733749

Strategy from Georg, long time Member of P123 and a very good Quant. Strategy is not (!) free, but still wanted to highlight this one:

Lovely Companies

https://www.portfolio123.com/app/r2g/summary?id=1715794

I love the name of that strategy. From Victor, not free, but nice :-)

Success in investing is not only about aiming for high ('risk-adjusted') returns. It is just as much about sticking to a process. This means you need to love the companies you invest in. You need to be able to trust your strategy. If you do, you are more likely to achieve those great returns you are looking for. 'Lovely Companies' does just that. It invests only in companies that give you peace of mind. More likely than not, the company will conduct activities that you can believe in. Also, when eyeballing their financials you will hardly ever have to scratch your head, and you will actually like what you see. The 'Lovely Companies' strategy might not have the highest returns around in the designer model marketplace, but you will definitely not regret investing in the companies it brings to your attention. So, say "no" to that cheap paper fabricant out in the Midwest that you would never want to buy in real life. Say "no" to the 'this can't be for real' cheap offshore drilling company located in the snowy weather of Alaska. Invest in the quality and 'lovely' companies that you want to buy. Within the world of lovely companies, a special focus is placed on the stability and the long-term growth prospects of the company. The universe consists of both US and Canadian companies with a minimum median dollar volume of 50.000 US dollars. Happy investing!

Urbem Quantitative Investing

https://www.portfolio123.com/app/r2g/summary?id=1570945

From Steven, not free (18$).

This is a concentrated portfolio strategy buying high-quality US-listed companies at sensible prices with infrequent rebalancing and the aim to beat the index for the long run with low costs and low risks. Check for more details on www.urbem.cn.

[Styles] - Profitability - Russell 1000

From Alan:

Strategy The "Styles" strategies target factors that have outperformed traditional indexes over long periods of time, as observed over decades of academic research, and are backed by a sound economic intuition or structural rationale, such as:

Risk premia, i.e., compensation for bearing risk;

Behavioral biases; and/or

Structural rationale, e.g., performance is typically measured versus a benchmark, which may cause investors to shun strategies with high tracking error to traditional cap-weighted indices.

The factors include:

Value investing targets companies that are relatively cheap, but may have higher risk of defaults or financial distress, and therefore carry a risk premium. Behavioral biases may also explain why value investing outperforms in the long run, such as the over-extrapolation of trends.

Profitability is a key component of "high-quality" companies, and a characteristic that investors should be willing to pay a premium for, all else equal.

Momentum is a style that invests in stocks with relatively higher price appreciation in the previous 12 months, and is an anomaly that can be explained by behavioral biases, such as an initial under-reaction to new information, and subsequent herding as the trend is identified.

Low Volatility targets securities with relatively low historical beta and volatility, measured as the standard deviation of returns. This anomaly can be explained by behavioral biases, such as a preference for lotteries and overconfidence. Benchmarking can also cause investors to shun low-volatility strategies, which typically exhibit high tracking error versus traditional market-cap weighted indices. Restrictions from utilizing leverage may also compel investors to overweight high-beta stocks in order to boost returns, which may lead to low-risk stocks being undervalued.

Investment is a relatively new factor, introduced by Fama and French in 2013, and targets companies that are more conservative in expanding book assets.

Because the Styles portfolios target single factors, they can be utilized in the following ways:

Benchmarking and attribution

Providing completion exposure to diversifying factors

Building a multi-factor book based on investor beliefs

Diversification and Capacity: The Styles strategies were designed to handle relatively high capacity, with reasonable turnover and broad diversification across many sectors and securities. Market Timing The strategy relies solely on bottoms-up stock selection, and does not employ any market timing, hedging or top-down sector/ETF allocation.

All right, what now?

Let us put all strategies into a strategy book (after ranking + a point in time database + cost averaging in systematic portfolios the second holy grail of systematic investing).

Here is a video on how to do this:

For Investors: How to build a Strategy Book with Time Tested P123 Portfolio Strategies

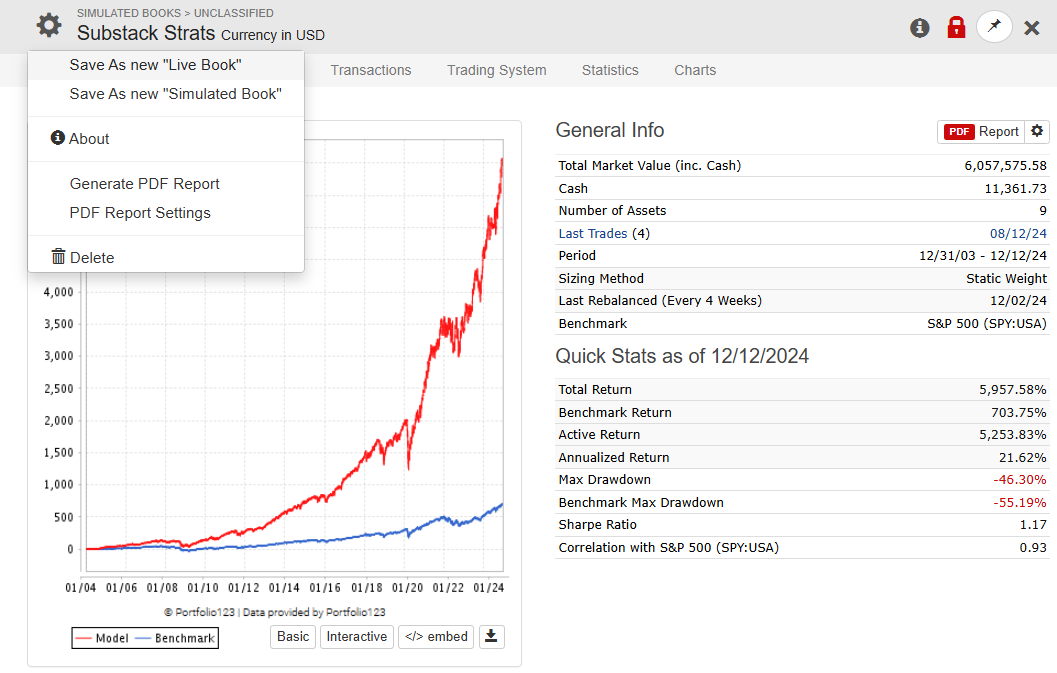

Here is the link to the strategy book https://www.portfolio123.com/port_summary.jsp?portid=1812900

Strategy Book

Not too bad. A Sharpe Ratio of 1.17.

All strategies are equally weighted in the above book + a 52 week rebalance of the weights of the strategies in the book.

All above strategies are accessible for a 25$ Subscription.

If you have the “Portfolio” Subscription, you can put the strategies into a simulated strategy book, save the strategy book as a live book (and do not have to calculate the exact weightings in Excel!).

Let us say you want to invest 100k into the strategy book. You define 100k + automatic rebalance:

Now —> the strategy book will run automatically and pick up the signals from the strategies within the book.

You will exactly know how much, and which shares to buy and sell every week systematically. Connect it to an Interactive Brokers account or tell your financial advisor to run it for you.

+ you can add BIL 0.00%↑ (short term bonds with no duration risk) to adapt it to your risk profile. Or add GLD 0.00%↑ for further diversification.

The sky is the limit ;-)

All the best and best regards.

Andreas

The information on from Andreas Himmelreich / QuantStrike and this video / blog is for information and discussion purposes only. It does not constitute a recommendation to purchase or sell any financial instruments or other products. Investment decisions should not be made with this video / blog, and one should consider the investment objectives or financial situation of any person or institution.

Investors should obtain advice based on their own individual circumstances from their own tax, financial, legal and other advisers about the risks and merits of any transaction before making an investment decision, and only make such decisions based on the investor’s own objectives, experience, and resources.

The information from Andreas Himmelreich / QuantStrike and this video / blog is based on generally available and paid information and, although obtained from sources believed to be reliable, its accuracy and completeness cannot be assured, and such information may be incomplete or condensed. All performance results are hypothetical and the result of back testing only. Out-of-sample performance may be different. No claim is made about future performance.

Investments in financial instruments or other products carry significant risk, including the possible total loss of the principal amount invested. Andreas Himmelreich / QuantStrike and this video / blog do not purport to identify all the risks or material considerations which may be associated with entering any transaction. Andreas Himmelreich / QuantStrike and this video / blog accepts no liability for any loss (whether direct, indirect or consequential) that may arise from any use of the information contained in or derived from Andreas Himmelreich / QuantStrike and this video / blog.

Thanks for this