My TA Patterns...

Pre stock selection, real time filter, the right environment (network momentum), industry group momentum + TA on the weekly and hourly (somehow the daily messes up my brain completly)...

This post is for documenting the momentum, breakout trading R&D (as I define it on the hourly).

Took a while, but I am getting some traction! I know: lot of stuff in one post, but I want to post a holistic view that does not left out important things.

So I cover pre stock selection, real time filter, the right environment (network momentum), industry group momentum + the weekly and hourly (somehow the daily messes up my brain completly) setup.

I read a ton of TA Books, I all put them aside and defined my own rules (which now look much like the TA Book stuff, lol), but I had to define them by myself, so I can spot them (TA Book setups never made sense to me in the heat of the battle).

For that I looked at 10.000s (or so) of charts and customzied the TC2000 charts for my (!) eyes.

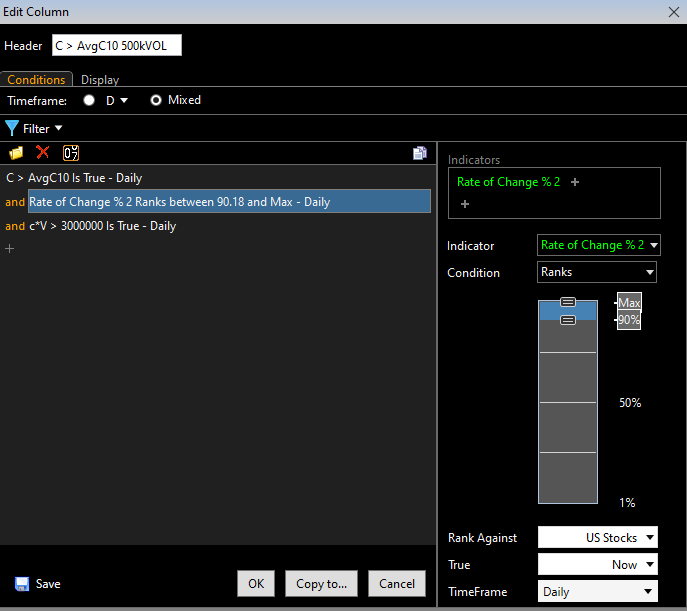

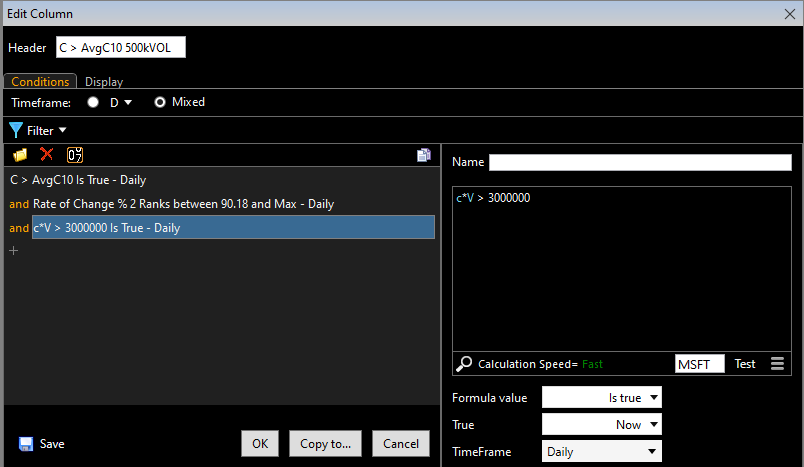

First of all, for stock selection I am using the following screens:

From what I see so far, preselection (fundamentals and technical) of the stocks you watch is very important: my best guess (I do not have the statistics long enough to prove it and yes it depends on the market environment): at the very least I want stocks that have improving earnings per share estimates, they can be trashy (e.g. have negative earnings, Rate of change up is the thing that matters here) as hell, but analysts need to upgrade them in terms of their earnings per share estimates. From what I saw so far (again still running the stats), those stocks “behave well” in terms of my risk preference.

The ranking system of the second screen is proprietary, but you can use the “Small and Micro Cap Focus” Ranking system (it also works and mid and big caps, if you want nullify the market cap stuff), it comes out the box with P123.

Those stocks move slower, and everybody knows they have good fundamentals, so not as much as convexity like in the first screen. But (!!!) they can be also great movers, if the industry group was neglected for months and now shows momentum.

Also if you get a GOAT big cap stock like NVDA or AMZN in the screen, pay attention, those big caps rarely get very high fundamental rankings, this is significant bullish (NFLX and APP (before the breakout, I just missed it ;-)) is in the above screen, META and NVDA was in it in 2023 pretty early on!).

+ the positions of that following system (mid and big caps, Russel 3000 Universe, growthy and yes, some higher beta (but not too high) is in play too!).

Now I copy the stocks from the screens and system(s) to TC2000 in different buckets…

[on the far left —> Industries with shorter term (!) momentum and relative strength —> best breakout stocks come from those Industries]

…and filter them real-time out with this real time screen:

((H - L + ABS(H - C1) + ABS(C1 - L)) / 2)*.9 >

(AVGH10.1 - AVGL10.1) / 2

+

(ABS(H1 - C2) + ABS(C2 - L1) +

ABS(H2 - C3) + ABS(C3 - L2) +

ABS(H3 - C4) + ABS(C4 - L3) +

ABS(H4 - C5) + ABS(C5 - L4) +

ABS(H5 - C6) + ABS(C6 - L5) +

ABS(H6 - C7) + ABS(C7 - L6) +

ABS(H7 - C8) + ABS(C8 - L7) +

ABS(H8 - C9) + ABS(C9 - L8) +

ABS(H9 - C10) + ABS(C10 - L9) +

ABS(H10 - C11) + ABS(C11 - L10)) / 20

and V > AVGV.10

_____________________________________________________________________

Now, before I put on breakout positions the environment must be right:

In general, I want to see network momentum be in the Quad 1-2 bucket, if in Quad 3 or 4, limit the breakout to those Quad 3 or 4 exposures (with smaller position sizes!):

Here is the filter I use (it is now based on daily network momentum, not weekly network momentum, also I look at the daily Rate of change, I might be risk on if Quad 1-2 is still in minority, but has positive ROC momentum, e.g. more Quad 1-2 exposures pop up than yesterday…):

Quad 1 exposures (in the Quad 1 Bucket)

iX2450

SVIX

KRE

XLF

iX2470

GBTC

SX30

QQQ

SX100

T2108

IXCO-X

NYFANG

RSP

IWM

iX2320

SX20

SX110

iX2270

ARKK

iX1020

iX1240

iX2380

iX2340

iX2330

iX2480

iX2370

iX2440

iX1170

IWC

Quad 2 positions:

iX2270

KWEB

SVIX

EUR/USD

IXCO-X

iX1080

GBTC

iX1130

SX30

PSCI

QQQ

NYFANG

iX1170

SX100

IWM

T2108

SX20

SX110

iX2470

iX2450

iX2440

iX2370

iX2480

iX2330

iX2340

iX2380

iX1240

iX1020

ARKK

iX2320

IWC

Quad 3 positions:

iX1050

SARK

SX10

RSP

iX1090

ZUQ.TO

iX1840

T2127

RWM

BRKB

URA

OIH

iX2030

UUP

IRX--X

SPBIO.X

SPXPV

TNX--X

XMI

T2108

T2104

T2100

SX90

iX1110

USO

XLE

iX1010

iX2260

XLU

SHY

Quad 4 positions:

iX1740

iX1730

XMI

T2104

T2100

T2127

XLP

IXR

PSQ

RWM

XLU

iX1100

SX50

VIXY

UUP

GLD

TLT

iX2290

iX1830

iX1770

iX1850

SX70

XLV

+ I love the GEX!

Basically, I try to spot divergences (Market down, GEX up would be a buy signal, Market up slightly, GEX up much as well and the other way around).

Quads + GEX —> defines risk on (take breakouts) or risk off (sit tight, manage positions).

Now the pattern comes in.

I want to see this:

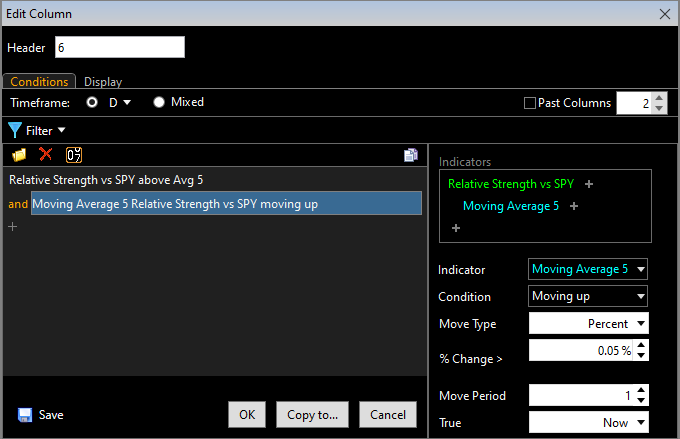

Blue line support on the weekly: I only choose stocks that hold the last major breakout bar (the low of it!).

The closer we are to the last blue bar weekly support, the more interested I am (e.g. I am buying mostly in a weekly pullback, if the environment is really strong + the base is 4 weeks long, I also consider typical breakouts above daily and weekly pivots. But let’s just say, I rather buy before “traditional” TA pivots.)

On IAG hourly —> (on the day I took it, Gold / Silver were the strongest industry groups).

I want to see blue bar support on the hourly:

Sell rules —> Stop loss is the low of the blue breakout candle and I move it up based on blue bar support…, position size is based on the stop loss I can put on, the higher the % of the stop loss, the lower my position (10% position on a 3% stop loss for example).

Here is the chart template: https://www.tc2000.com/~zJaV2C

The whole setup in TC2000 looks like this: https://www.tc2000.com/~4JBn9Z (template)

The template for the Quads looks like this: https://www.tc2000.com/~TwLGbo

(you must copy the Quad exposures to the corresponding Quad baskets, TC2000 does not copy them for you in the template).

That is it ;-)

All the best and best regards

Andreas

The information on from Andreas Himmelreich / QuantStrike and this video / blog is for information and discussion purposes only. It does not constitute a recommendation to purchase or sell any financial instruments or other products. Investment decisions should not be made with this video / blog, and one should consider the investment objectives or financial situation of any person or institution.

Investors should obtain advice based on their own individual circumstances from their own tax, financial, legal and other advisers about the risks and merits of any transaction before making an investment decision, and only make such decisions based on the investor’s own objectives, experience, and resources.

The information from Andreas Himmelreich / QuantStrike and this video / blog is based on generally available and paid information and, although obtained from sources believed to be reliable, its accuracy and completeness cannot be assured, and such information may be incomplete or condensed. All performance results are hypothetical and the result of back testing only. Out-of-sample performance may be different. No claim is made about future performance.

Investments in financial instruments or other products carry significant risk, including the possible total loss of the principal amount invested. Andreas Himmelreich / QuantStrike and this video / blog do not purport to identify all the risks or material considerations which may be associated with entering any transaction. Andreas Himmelreich / QuantStrike and this video / blog accepts no liability for any loss (whether direct, indirect or consequential) that may arise from any use of the information contained in or derived from Andreas Himmelreich / QuantStrike and this video / blog.