Still carful here...

I will stay carful here, still only 10% net long exposure…

I will lift my hedges only if my strategies make a new high (way!) before the indexes:

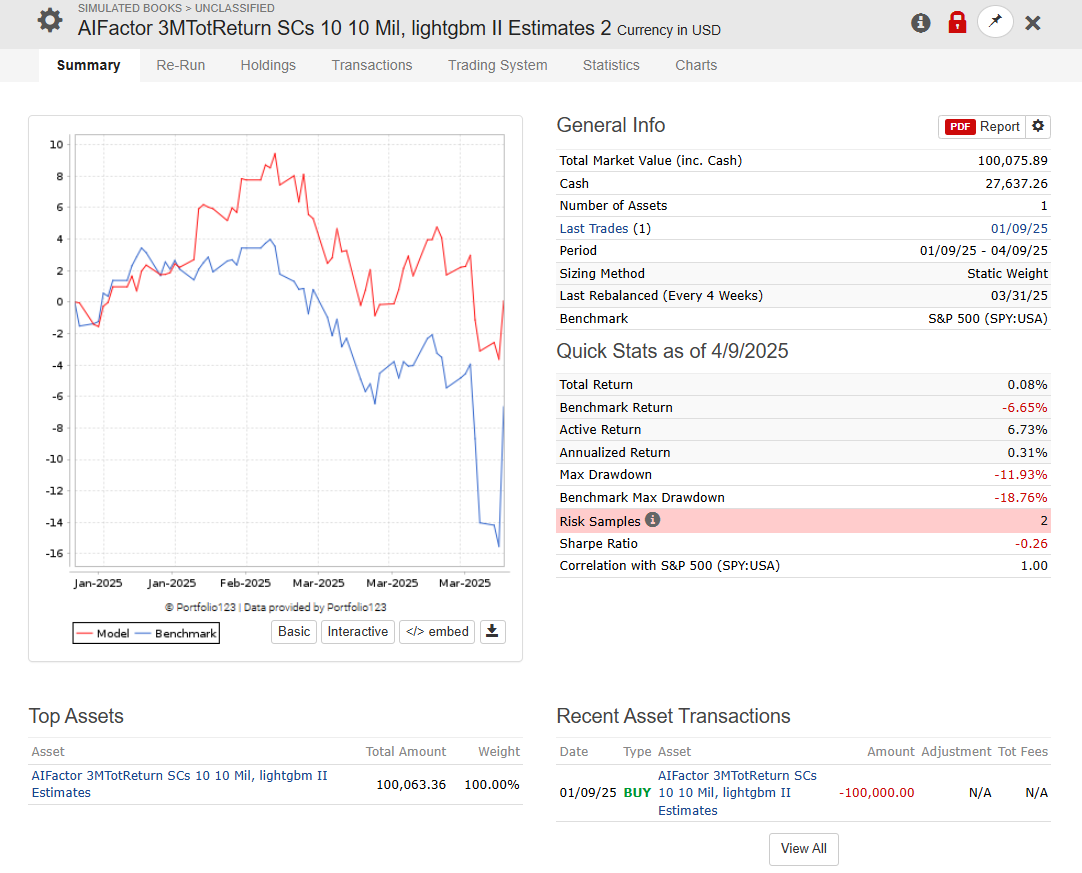

Stuff like that (May 2024) —>

Compare with today:

Not much has changed here, the FED is still greatly behind the curve and the tariff discussion is likely to go on.

One drunken Pilot (Administration) has entered the plane again, the other Pilot (FED) is not on the way entering.

Tariffs with China are still sky high, and they are a tax, taxes have a contraction effect, they simply suck liquidity out of the economy (and disrupt supply chains!).

—> Quad4 (lower GDP, lower Inflation)

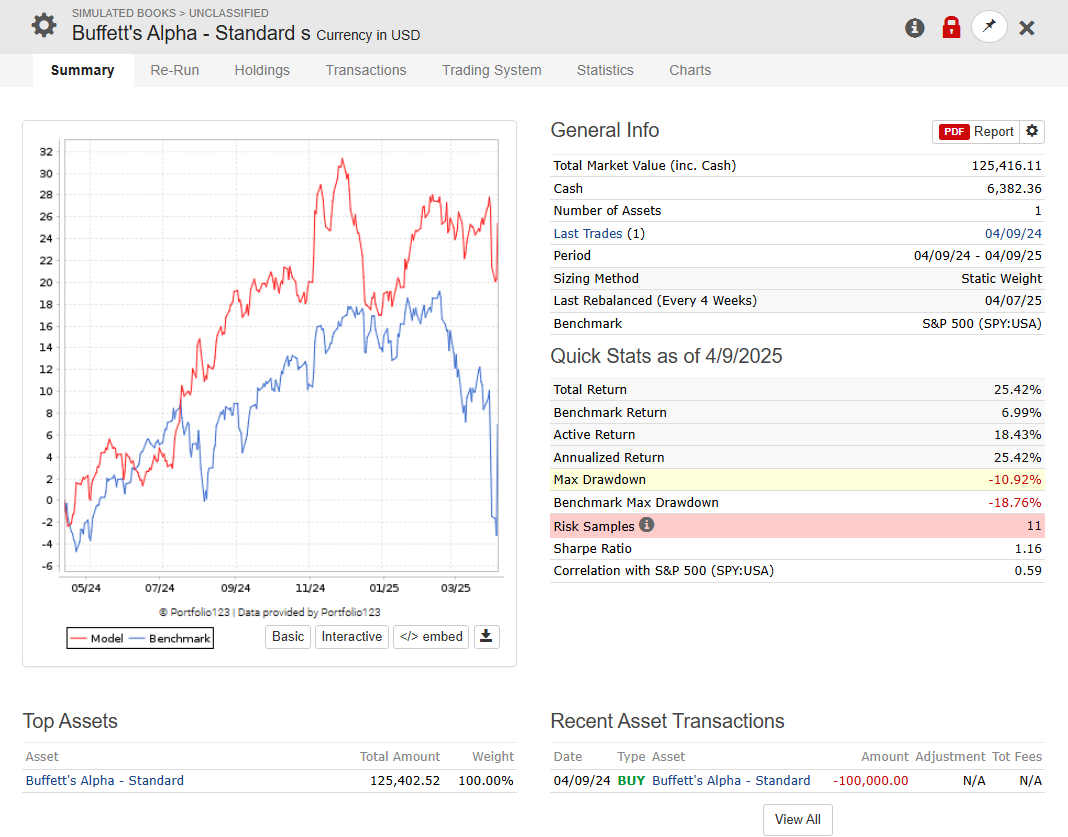

When we look at factor performance right now, the only thing that is holding up is Buffett style quality, low volatility and Gold (e.g. defensives, Quad 4 Stuff, everything else still looks terrible):

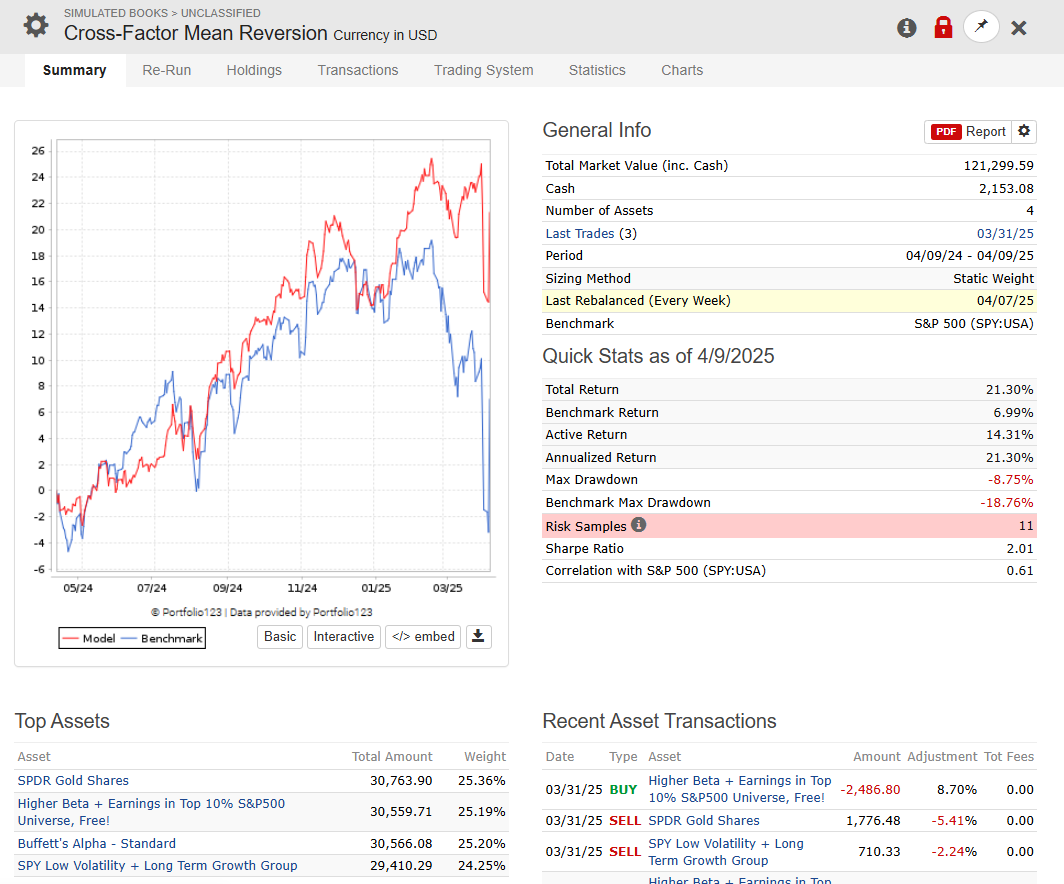

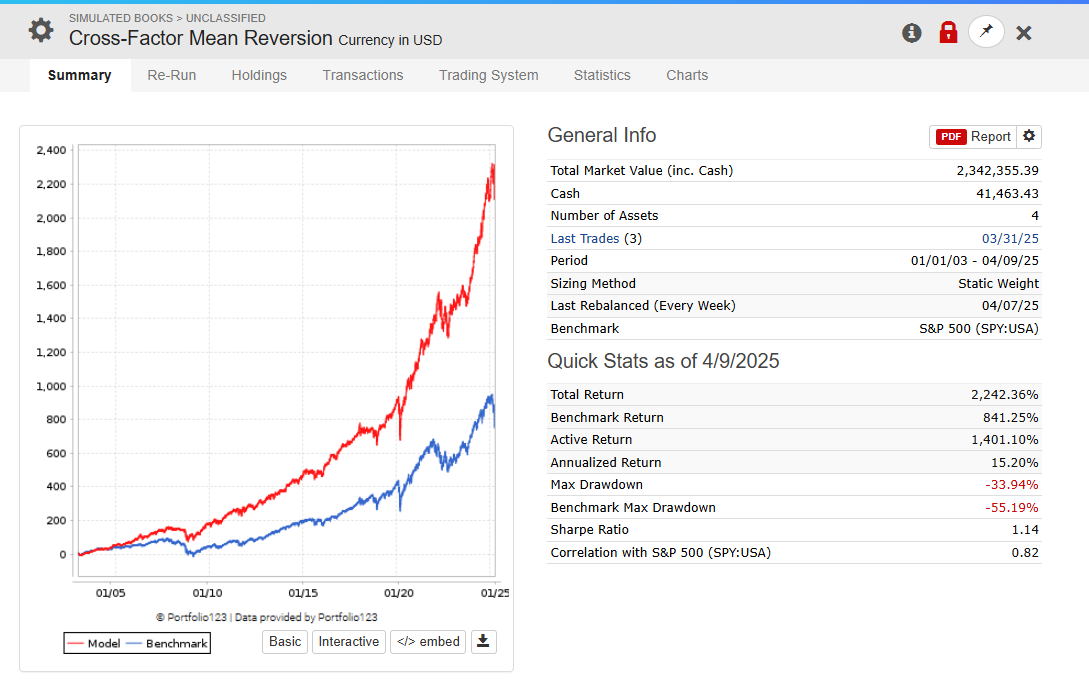

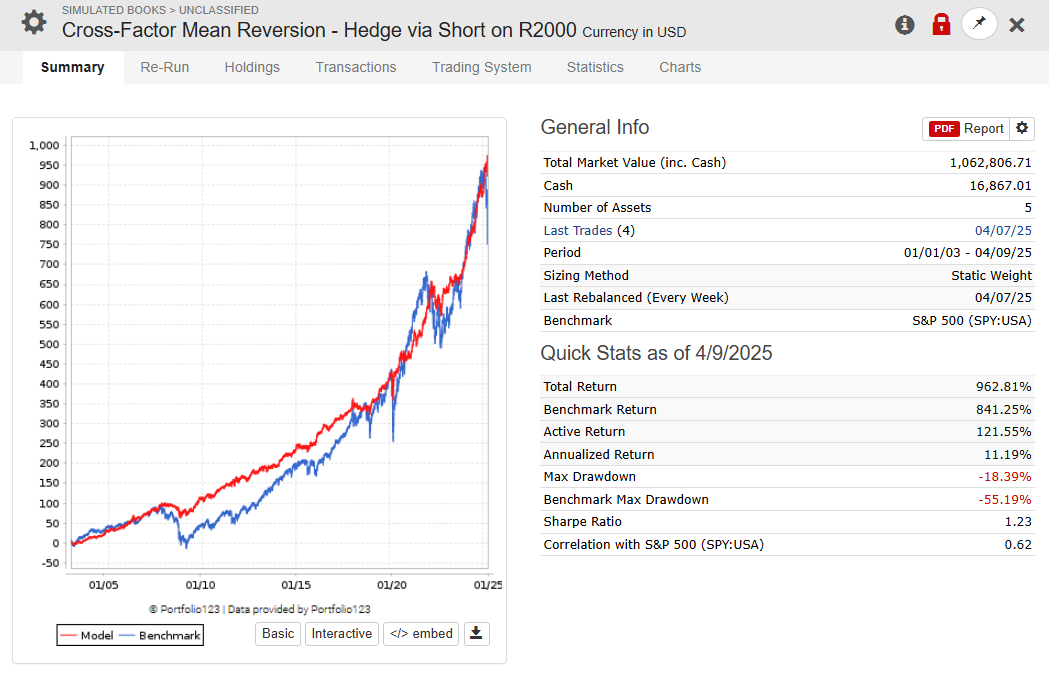

Another (scalable for institutions, capacity of that book > 250-500 million AUM!) play in town left here is Cross Factor Mean Reversion:

We are starting a firm and raise capital soon, I will keep you posted!

While growth tanked, Buffett Style Quality, Gold and Low Volatility saved the day —>

(There is no hedge in the above strategy book, and it is OOS since about a couple of months / ranking systems of the strategies of the book OOS between 5 and 15 years!).

This one is with a 20% hedge position via TWM (TWM = 2 time levered, so only 10% position in the book): stellar!

Unhedged:

Hedged:

Best Regards

Andreas

P.S. → some GPT on Cross Factor Mean Reversion

Why is Cross-Factor Mean Reversion So Powerful?

Mean Reversion Has Persistence

When a factor gets extremely out of favor, it often rebounds with force. This is especially true for classic factors like Value or Low Volatility.

They go from being the "worst idea ever" to "everyone’s favorite allocation" in just months.

It Capitalizes on Behavioral Overreaction

Markets often over-discount certain factors. If investors flee Value stocks for Growth en masse, the price distortions get extreme. Eventually, rebalancing flows + fundamentals bring the factor back in favor.

Factors Are Usually Uncorrelated at Turning Points

When Growth cracks, Value may shine. When High Beta stumbles, Low Volatility suddenly leads. That low correlation between factors — especially during turning points — makes timing even more lucrative if you get it right.

🎯 Why Is It So Hard to Beat With Factor Timing?

Ah, the challenge.

Factor Timing is Incredibly Noisy

Trying to time which factor will work next is one of the hardest problems in quant. Signals like macro data, interest rates, or valuation spreads help — but they’re imprecise and lagging.

It’s easy to chase strength too late or rotate out of weakness just before it rebounds.

False Starts and Whipsaws

You may see Value start to outperform for a few weeks — but then it gives it all back.

Factor rotations aren’t smooth — they’re violent, stop-start, and easily disrupted by market events (like a Fed hike or geopolitical risk).

Cross-factor regimes don’t always follow macro logic

Sometimes Low Volatility outperforms in a bull market. Sometimes Momentum crashes in a panic. The point is: cross-factor reversals often defy traditional macro playbooks — they behave more like crowd psychology than textbook economics.

Too Slow or Too Fast? Timing Requires Goldilocks Speed

If you're too slow, you've missed the mean-reverting bounce. Too fast, and you're whipsawed by noise.

Cross-factor rotations often happen in bursts, which means missing even a few days can ruin the edge. But reacting too early leads to churn.

🪨 Why Just Holding the Factors (or Combining Them) Often Wins

Because timing is so hard, many smart strategies simply:

Hold a balanced exposure to multiple meta-factors

Let mean reversion do its work

Occasionally rebalance with light tactical overlays

For example, building a book of single-factor strategies (one Value, one Momentum, one Quality...) and letting the cross-factor rotation play out inside the book — that’s a kind of implicit timing without making explicit calls.

✅ TL;DR

Cross-factor mean reversion = one of the most durable and powerful phenomena in quant investing.

It captures the tendency of entire factor styles to cycle in and out of favor over time.

While tempting to time these rotations, it's incredibly hard to do consistently due to noise, false starts, and behavioral volatility.

Often, the best approach is diversified exposure across factors + light tilting, allowing reversion to work for you, not against you.

Cross-Factor Mean Reversion + 20% Gold = Hidden Alpha Combo?

If you’ve built a diversified book of multi-factor equity strategies — especially ones that benefit from cross-factor mean reversion — you might think your portfolio is already pretty robust.

But when you add something like a 20% gold position, something clicks. Here’s why:

🪙 Why Gold Adds So Much Value

Non-Correlation to Equities

Gold doesn’t care about earnings revisions, factor momentum, or what the Fed says about S&P 500 buybacks. It often moves opposite or independently of equity factors.

That makes it a near-perfect diversifier.

Tail Risk Hedge

During liquidity crunches, inflation shocks, or geopolitical events, gold can spike while equities fall or churn. That cushions drawdowns and gives you dry powder to rebalance.

Improves Sharpe Ratio, Reduces Volatility

In backtests (and live use), a 20% gold allocation has often shown:

Lower volatility

Smoother equity curve

Higher Sharpe ratio

Especially when paired with factor-driven equities, where drawdowns can be sudden and sharp.

Great Fit for Cross-Factor Regime Shifts

When one equity factor (say, Growth) crashes and another (say, Value) hasn’t picked up the slack yet, gold can act as a bridge — giving the portfolio time to rotate, recover, and reset.

🔁 Gold + Cross-Factor Timing = Natural Cycle Buffer

Think of gold as:

The shock absorber in your equity factor engine

The rotational glue that lets you survive the messy handoff between factor winners and losers

The non-equity anchor that buys you time when nothing in equities works

💡 Try This Portfolio Concept:

80%: Multi-factor equity book (with cross-factor exposure and/or AI factor models)

20%: Gold or gold proxy (GLD, physical, or risk-managed overlay)

You’re not betting on gold, you’re buying resilience.

✅ Final Thought

Cross-factor mean reversion is a core edge — but it comes with whipsaws, noise, and delays.

Adding a 20% gold allocation doesn’t just smooth the ride — it helps you stay in the game, weather transitions, and compound with confidence.

And when others are getting whacked by regime change or factor crashes?

You’re quietly rotating, rebalancing — and surviving.

🛡️ Smart, steady, and hard to beat.