The Great Mindset Shift: Why "Debasement" is Replacing "Deflation" as the Market's Driving Fear

...and what it means for Factor Investing!

For decades, the ghost haunting the halls of central banks and retirement portfolios was deflation — a sustained drop in prices that cripples growth and emboldens creditors. The investor’s primary fear was the permanent impairment of capital, the loss of principal.

But in 2025, a profound shift is accelerating. The dominant fear is no longer losing your initial investment; it’s watching your capital stagnate while the world prices ahead of you. The fear of losing purchasing power is decisively replacing the fear of losing principal.

This isn’t just a philosophical change. It’s a tectonic shift in market psychology that is actively reshaping market structure and consumer behavior right now. The first half of 2025 has turbocharged the transition from a “deflation” to a “debasement” mindset.

The Old World: The Deflationary Playbook

The post-GFC era was defined by the fight against deflation. Investor behavior adapted accordingly. The “Safety” Trade was a relentless bid for government bonds as the cornerstone of portfolios. Capital preservation was paramount; “return of capital” was prioritized over “return on capital,” and cash was king. Unexceptional companies could thrive in a zero-rate world where any yield was a good yield. Market leadership came from low-volatility, high-dividend, and quality stocks as investors sought steady, defensive returns. The system was wired for stability, and the biggest risk was a sudden crash that could wipe out your nest egg.

The New Regime: The Debasement Imperative

The new regime is defined by the persistent erosion of fiat currency value through fiscal largesse, reshored supply chains, and structural inflation. The investor’s calculus has flipped. The question is no longer “How do I protect my money?” but “Where must I put my money to protect its value?”

This manifests in two powerful ways.

In Market Structure, we see a structural bid for real assets with intrinsic, finite value — gold, commodities, and energy—that cannot be printed by a central bank. They are no longer just inflation hedges; they are core holdings in a debasement portfolio. The old “bond proxies” like slow-growth utilities and slow-growth consumer staples are suffering, as their steady but low growth cannot outpace inflation, making them a guaranteed path to lost purchasing power. Furthermore, in a world of debasement, the real value of debt declines over time, encouraging corporate and individual risk-taking and fueling investment in productive capacity and speculative assets. This also leads to capital funneling into companies that enable efficiency and automation — the only true long-term antidote to inflationary pressures.

In Consumer Behavior, the psychology of stagflation is creeping back. Consumers are increasingly forward-purchasing durable goods, locking in mortgage rates, and making long-term investments now, anticipating higher future costs. The erosion of cash hoarding is another key sign; the mattress is no longer safe. Savers are being forced into the market, not out of greed, but out of necessity, becoming reluctant, risk-tolerant investors by circumstance. This behavior also exacerbates inequality, creating a bifurcated economy where those with assets that appreciate with inflation pull further away from those whose primary asset is their labor, which often lags price increases.

What This Means for Factor Investing

The transition from a deflationary to a debasement regime doesn’t just change asset allocation — it rewires the factor landscape. The “slow and steady” factors that thrived in a zero-rate world are being supplanted by those that can harness or protect against the erosion of purchasing power.

Short-term momentum and earnings revisions will become more crucial than long-term quality, as they capture the immediate re-pricing of assets and real-time changes in a company’s fundamental outlook in a fast-moving environment. The market will reward current acceleration over pristine balance sheets.

Value gets a new lease on life, but with a twist. Traditional book-value metrics may be misleading. The new “debasement value” will be found in factors like Cash Flow Return versus Enterprise Value and Free Cash Flow Yield — metrics that measure a company’s ability to generate real cash returns today, not the accounting value of its legacy assets.

Conversely, we will likely see the decline of low volatility and pure defensives without earnings acceleration.

In essence, the factor playbook is flipping from defense to offense. The premium will be on factors that benefit from rising nominal prices, capture immediate cash flow, and represent claims on scarce resources. The era of debasement is an era for dynamic, real-return-focused factors.

Factors that will do well!

1. Pricing Power & Real Earnings Growth

These factors identify companies that can pass on rising costs and generate true, inflation-adjusted profit growth.

SalesGr%TTM and OpIncGr%TTM: Strong, recent sales and operating income growth.

%(SalesGr%TTM, SalesGr%3Y): Sales Growth Acceleration, indicating improving momentum.

LoopSum(”Sales(CTR,TTM) > Sales(CTR+1,TTM)”,20): Quarters of Sales Growth 5Y, demonstrating a long track record.

EBITDAYield and EarnYield: High earnings and EBITDA yields signal robust current profitability relative to price.

2. Scarcity & Tangible Asset Value

These factors target companies with real, hard assets or exposure to rising commodity prices.

InventoryGr%TTM: In an inflationary environment, rising inventory values can be a positive, indicating goods are worth more.

FCFYield and NetFCFPSTTM / Price: Free Cash Flow Yield. Cash flow is a real, tangible output that can be reinvested or returned to shareholders.

Buyback Yield and ShareholderYield: Companies returning cash to shareholders are effectively converting corporate cash into real ownership.

3. Short-Term Momentum & Earnings Revisions

In a fast-moving regime, the market’s focus shortens. These factors capture immediate, high-conviction signals.

Surprise%Y1 and SUEY1: Recent earnings surprises indicate the company is beating expectations in the current environment.

%(CurQEPSMean, CurQEPS13WkAgo): EPS Est Current Q vs. 13 Wk Ago. The most powerful short-term signal of improving fundamentals.

%(CurFYEPSMean,CurFYEPS8WkAgo): EPS Est Current Yr vs. 8 Wk Ago. Rising full-year estimates show sustained confidence.

Up-Down EPS Revisions Net 75 days: Captures the net breadth of analyst upgrades versus downgrades.

Ret%Chg_D(65) (3M Return) and Ret%Chg_D(130) (6M Return): Price momentum confirms the fundamental story is being recognized by the market.

4. Relative Strength & Trend

These factors help avoid value traps and identify stocks that the market is favoring in the new regime.

% from 52Wk Hi: Stocks near their highs show strong relative strength.

Rel%Chg_D(260,#Sector) and Rel%Chg_D(260,#Industry): 12M Return vs. Sector/Industry. Identifies leaders within their peer group.

Close(0)/SMA(200) and Close(0)/SMA(50): Trading above key moving averages confirms a healthy medium-term trend.

On Value: The Right Way to Measure It Now

The classic value factor, often defined by backward-looking metrics like Price-to-Book, has struggled for years. Many have declared it dead. They are wrong, but they are using the wrong tools. In a debasement environment, the market is not pricing assets based on their historical accounting value, but on their future ability to generate real cash flows. The key is to use forward-looking value metrics grounded in earnings power.

Static book value is an anchor to the past. It fails to capture the reality that a company’s true worth lies in its discounted future earnings stream. When inflation is reshaping the economy, last year’s balance sheet is a poor guide. The market is forward-looking, and your value metrics must be too.

This is where earnings estimates become the critical differentiator. A stock trading at a low multiple to its forward earnings estimates is not just statistically cheap; it is fundamentally mispriced relative to its near-term profit potential. This creates a powerful catalyst. As those estimates are revised upward — a key signal in our process— the market is forced to reprice the stock to align with its new, higher expected cash flows.

Therefore, value is far from dead. It has simply evolved. The most potent form of value in today’s market is a combination of a low price relative to forward earnings estimates and positive earnings revision momentum. This “value with a catalyst” is immune to value traps and perfectly positioned to thrive in an environment where the premium is on tangible, near-term profitability.

https://www.portfolio123.com/app/ranking-system/509310

Factors to Be Wary Of

Pure “Low Volatility”: While stable, it may not provide the necessary return to outpace inflation.

Static High Dividend Yield: Can be a trap if the dividend is not covered by growing cash flows.

Traditional Book-to-Price Value: Book values are backward-looking and may not reflect replacement cost in an inflationary world. Tangible Book to Price is better, but cash flow-based value metrics are superior in this context.

+ The Gold Bull Market is Not Over

It is a mistake to view the recent rally in gold as a short-term spike. What we are witnessing is the early stages of a sustained bull market, fundamentally driven by the global shift into a debasement regime. Gold is not rising in a vacuum; it is reasserting its historical role as a store of value in the face of synchronized currency erosion.

The key driver is not just inflation, but a crisis of confidence in the traditional anchors of the financial system. For decades, sovereign bonds, particularly U.S. Treasuries, served as the ultimate safe asset. This is no longer the case. As major central banks and governments engage in unprecedented fiscal and monetary expansion, the real return on sovereign debt has collapsed, and in many cases, turned deeply negative. Gold, which carries no counterparty risk and cannot be printed, is the direct beneficiary of this structural shift. It is becoming the neutral reserve asset in a world where all fiat currencies are in a race to the bottom.

Furthermore, the buying base for gold has fundamentally expanded. It is no longer just a fear trade for retail investors. Central banks, particularly in the East, are buying gold at a record pace to diversify away from the U.S. dollar. This creates a persistent, structural bid that did not exist in previous cycles. For the individual investor, gold is no longer a speculative hedge; it is a core, strategic holding for capital preservation. Until the forces of fiscal and monetary discipline return—a distant prospect—the path of least resistance for gold remains higher. This bull market is a function of a changing monetary order, and it is far from over.

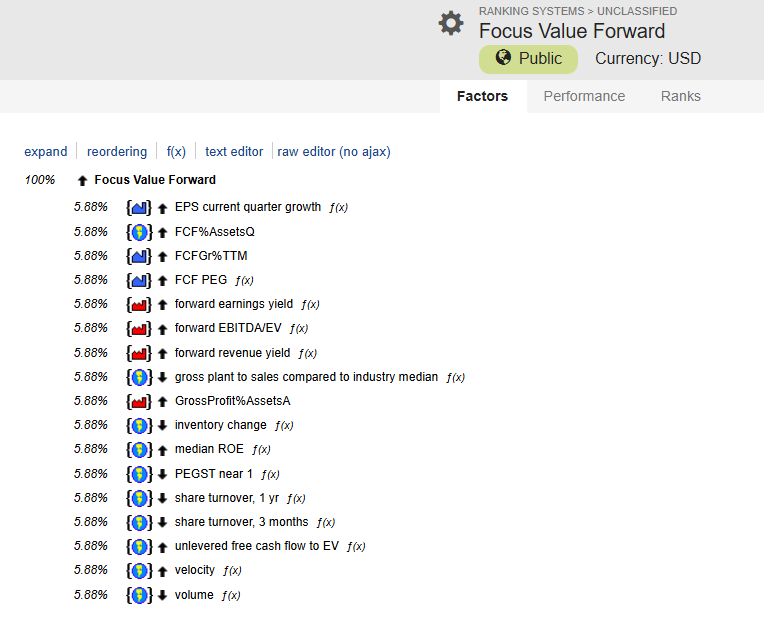

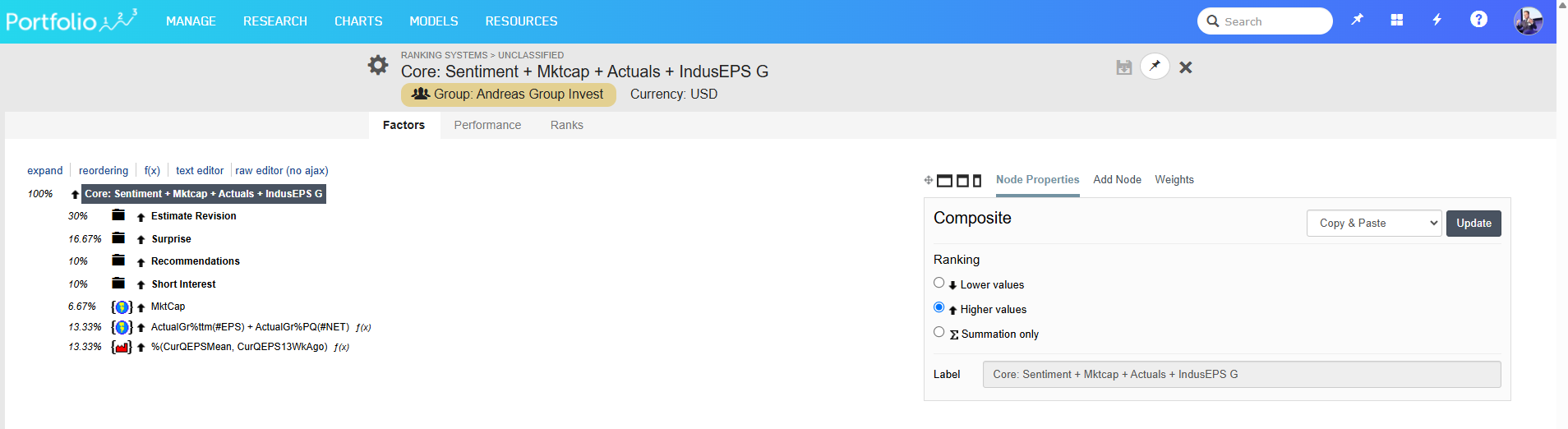

Portfolio123 Core Sentiment is a good start

Use it as a base and add factors.

Here is one example:

https://www.portfolio123.com/app/ranking-system/507188

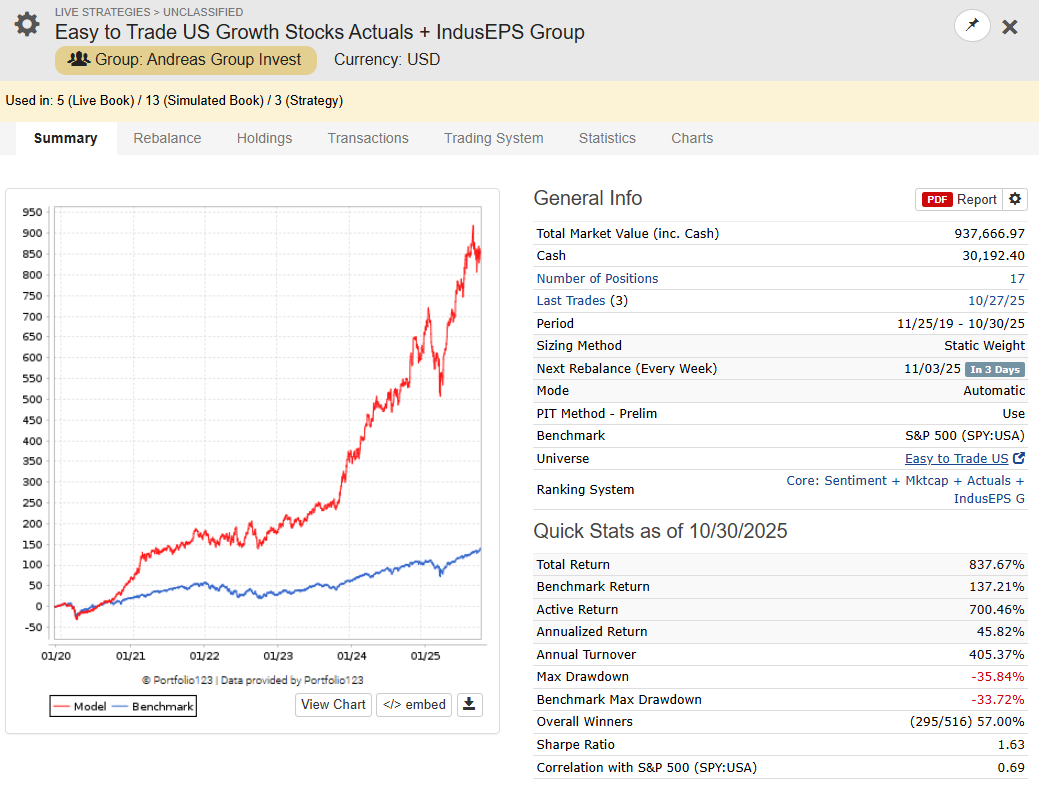

https://www.portfolio123.com/port_summary.jsp?portid=1815750

Best Regards

Andreas