🚀What Is Cross-Factor Mean Reversion? And how do you get rich the boring way?

What Is Cross-Factor Mean Reversion?

Most investors think about mean reversion as a single-stock phenomenon:

“This stock is down too much, so it will probably bounce.”

That’s not what we do.

Cross-Factor Mean Reversion works differently — and it’s far more powerful.

The Core Idea

We don’t mean-revert stocks.

We mean-revert factors.

Here’s how it works.

When Growth is hot, everyone chases it. When it cools, everyone sells.

Value is loved in some years, hated in others.

Low Volatility can be ignored for a decade — until suddenly it’s the only thing working.

Quality looks boring, until it’s the last man standing.

We hold all of them — always.

Not because we know which will work next.

Because we know they take turns.

The Mechanism

When Growth runs up fifty percent, we let it ride — but we rebalance.

When Growth corrects twenty percent, we trim less and let other sleeves catch up.

When Low Volatility struggles for years, we keep holding — because now it’s cheap.

When Low Volatility suddenly works, we’re already there. No chasing needed.

We’re not timing.

We’re structuring.

Why “Cross-Factor”?

Because the reversion happens across factors, not within them.

Single-factor thinking asks: “Is Growth overvalued?”

Cross-factor reality says: “Growth is expensive, Value is cheap — we own both.”

Single-factor thinking asks: “When will Low Vol work?”

Cross-factor reality says: “No idea. So we never sell it.”

Single-factor thinking asks: “Should I add Quality now?”

Cross-factor reality says: “Quality is always there. That’s the point.”

You don’t need to know what’s next.

You just need to own what will be next — before it is.

How This Works in Our Strategy Portfolio (=Strategy Book)

One sleeve captures upside when risk is on — Growth and High Beta.

Another owns companies that survive anything — Quality Value.

A third anchors the book when panic hits — Low Volatility.

And Gold hedges what no one can predict.

None of these work all the time.

Together, they work over time.

Access via free Research Group

Be a member of my free research group to get above’s strategy book:

https://www.portfolio123.com/app/group/317/home

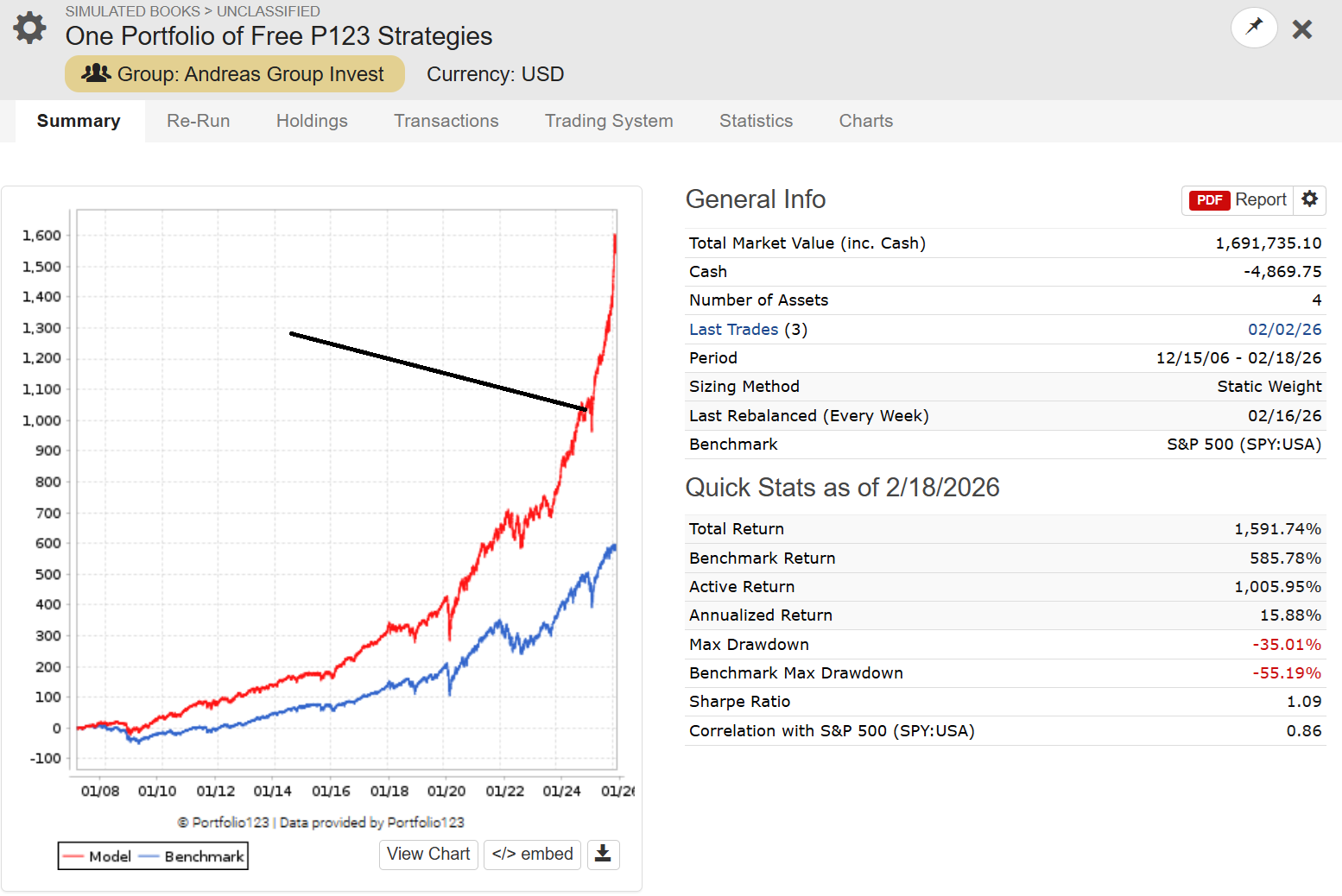

The Free Portfolio Proof

https://www.portfolio123.com/port_summary.jsp?portid=1853788

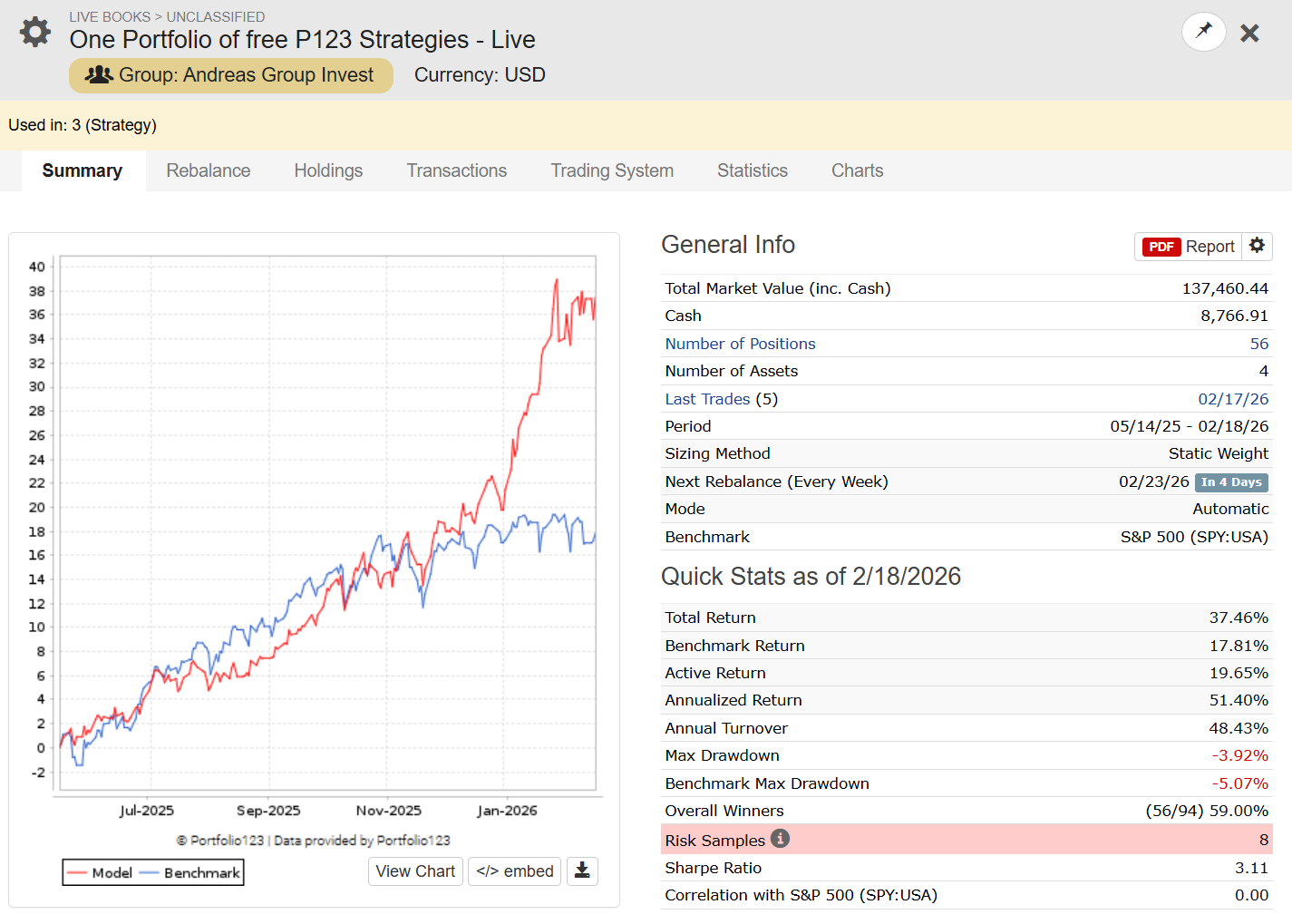

I build the book around October 2024, so the whole book is OOS (e.g. Live Trading, not a backtest!) since then.

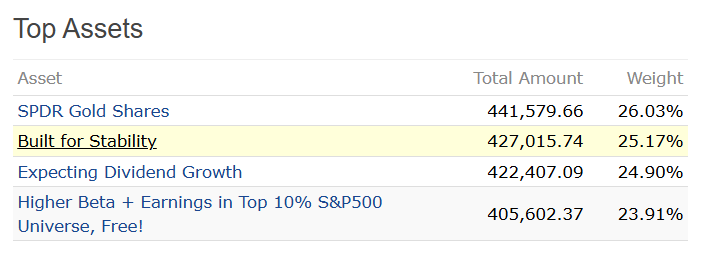

It contains the following strategies + a Gold ETF (equally 25% weighted!) —>

https://www.portfolio123.com/port_summary.jsp?portid=1503605

This one is OOS since 09/01/2017 !!!

(“Andreas, Dividend Stocks will never be back” ;-))

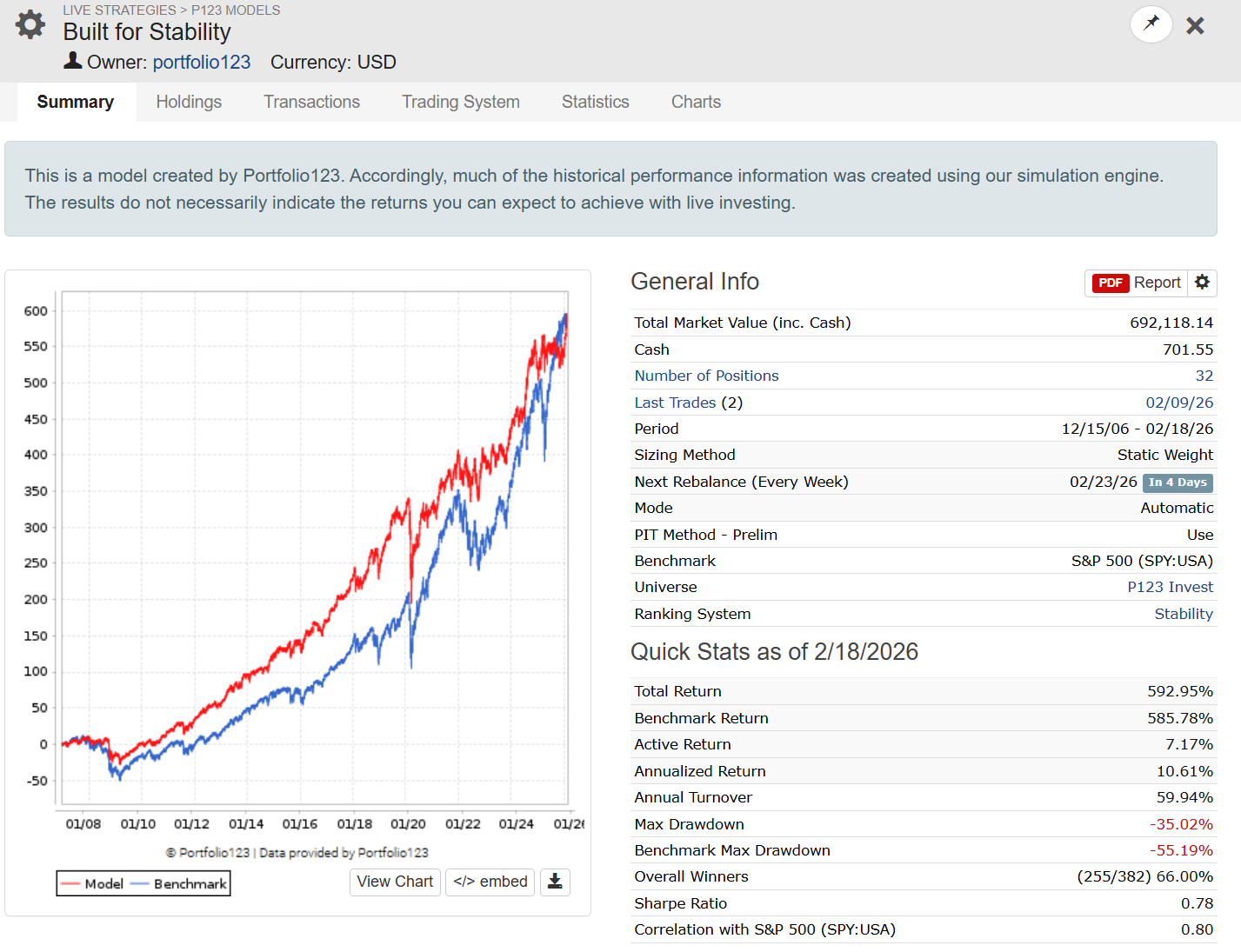

Here is Stability ;-) OOS since 12/09/2016

https://www.portfolio123.com/port_summary.jsp?portid=1457941

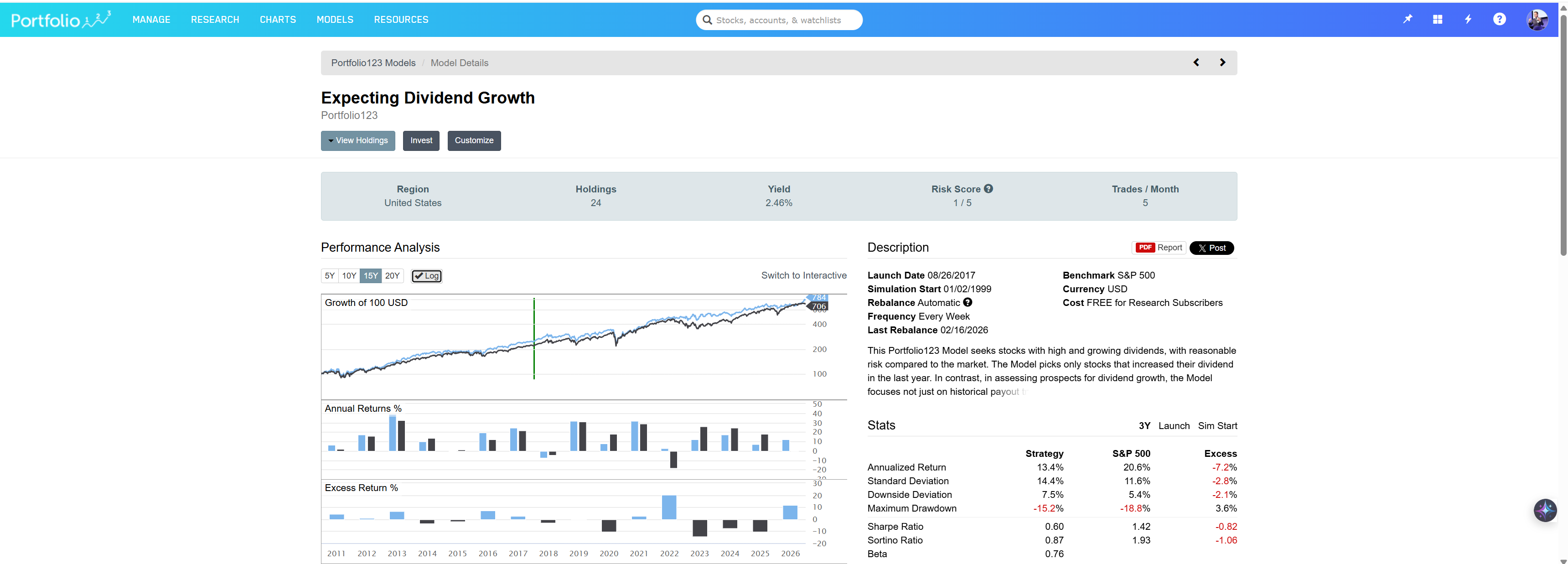

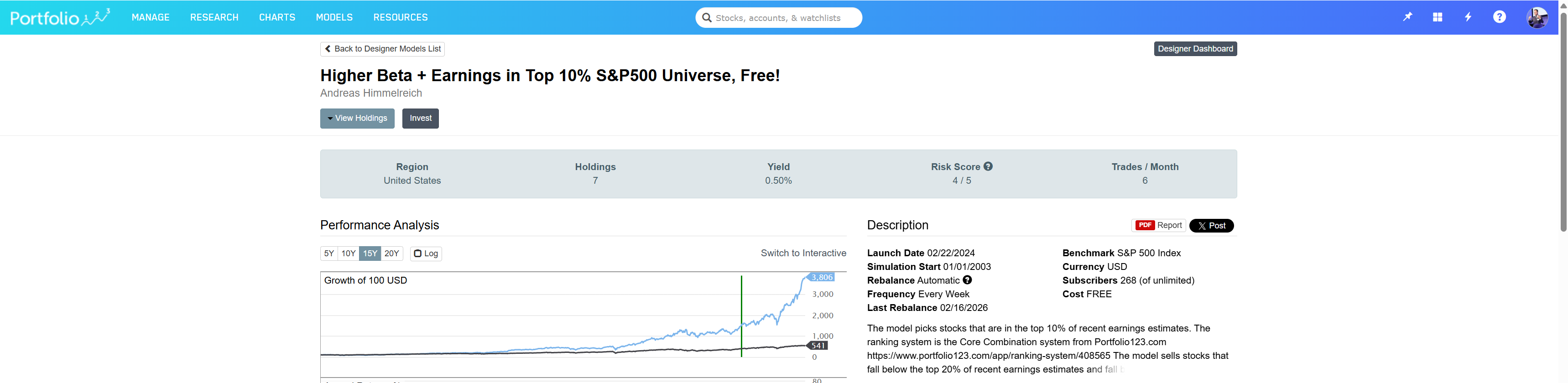

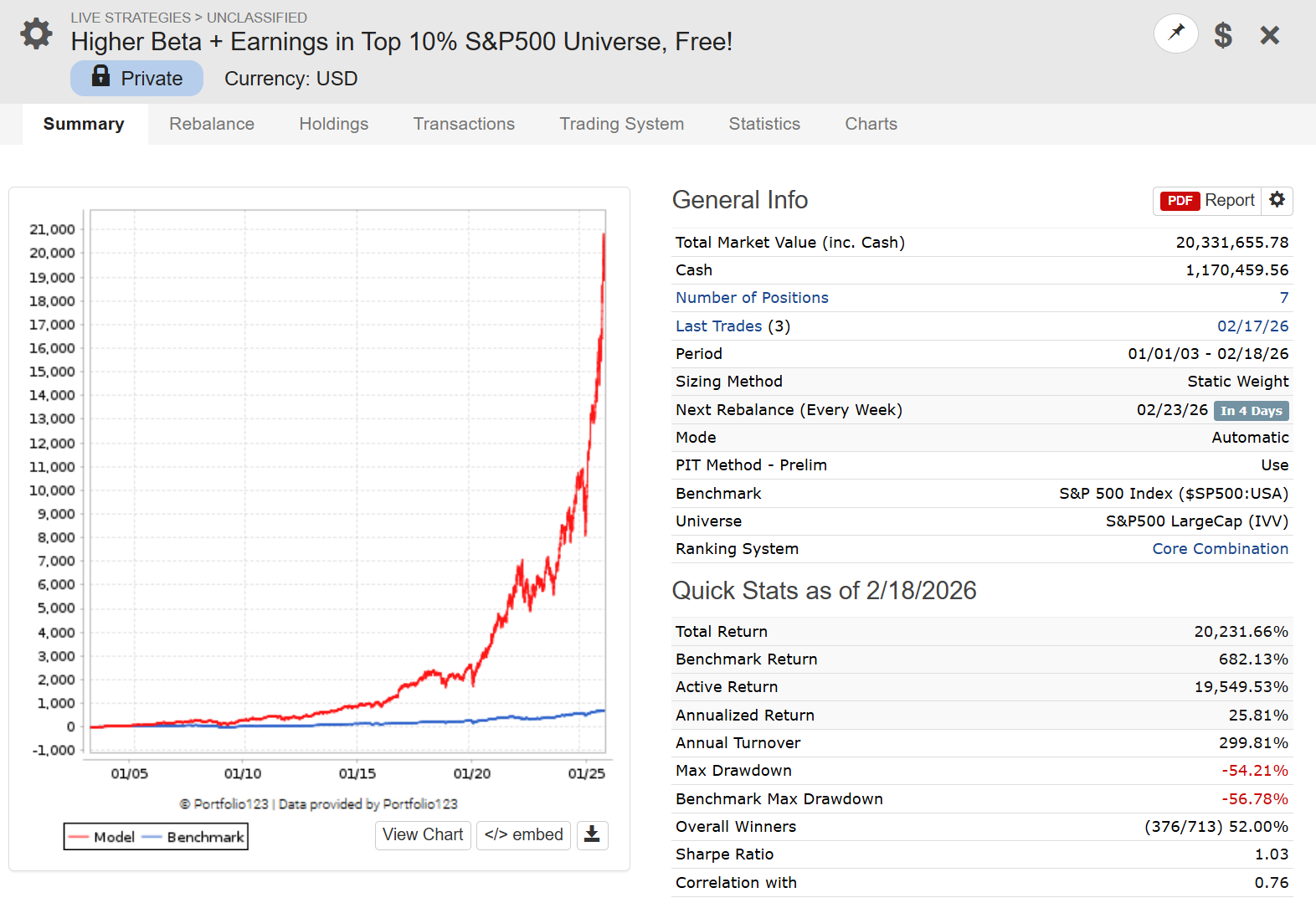

Yes, yes, yes, and here is growth (we need it ;-))

https://www.portfolio123.com/app/r2g/summary?id=1765750

Live Portfolio (connect P123 to Interactive Brokers and semi automate trading it!)

https://www.portfolio123.com/port_summary.jsp?portid=1854427

This is not luck.

This is Cross-Factor Mean Reversion doing exactly what it’s designed to do:

Capture upside when it’s there

Protect when it’s not

Never rely on being right about the next regime

Why 25% Gold? The Anchor That Makes the Book Work

In a book built on Cross-Factor Mean Reversion, every sleeve has a job.

Growth captures upside when risk is on. Quality owns companies that survive anything. Low Vol anchors the book when panic hits.

And Gold?

Gold is the structural hedge that ties it all together.

The Data Behind a 25% Gold Position

Research consistently shows that gold in the 20–25% range hits a structural sweet spot .

Portfolios with this allocation have historically posted higher risk-adjusted returns than all-equity allocations, not because gold outperforms, but because it smooths the ride.

Over more than fifty years, gold has demonstrated minimal correlation with stocks and bonds . VanEck’s data puts the long-term correlation between gold and the S&P 500 at essentially zero . That is not a hedge. That is a separate return stream entirely.

In every major crisis — the dot-com bust, the Global Financial Crisis, COVID — gold either held its value or gained while equities plunged . That is not timing. That is structure!

Why Traditional Ranking Systems Are the Perfect Tool for this!

You do not need machine learning for this. You need intentional construction.

With traditional ranking systems, you can build a Growth sleeve that ranks by momentum and earnings acceleration. You can build a Value sleeve that ranks by forward earnings and industry-relative metrics. You can build a Low Vol sleeve that ranks by beta and volatility. You can build a Quality sleeve that ranks by profitability and return on equity. And you can add Gold or other uncorrelated assets as a true diversifier.

Each sleeve is transparent. Each has a clear job. Together, they form a strategy book that does not care which factor is leading — because it owns them all.

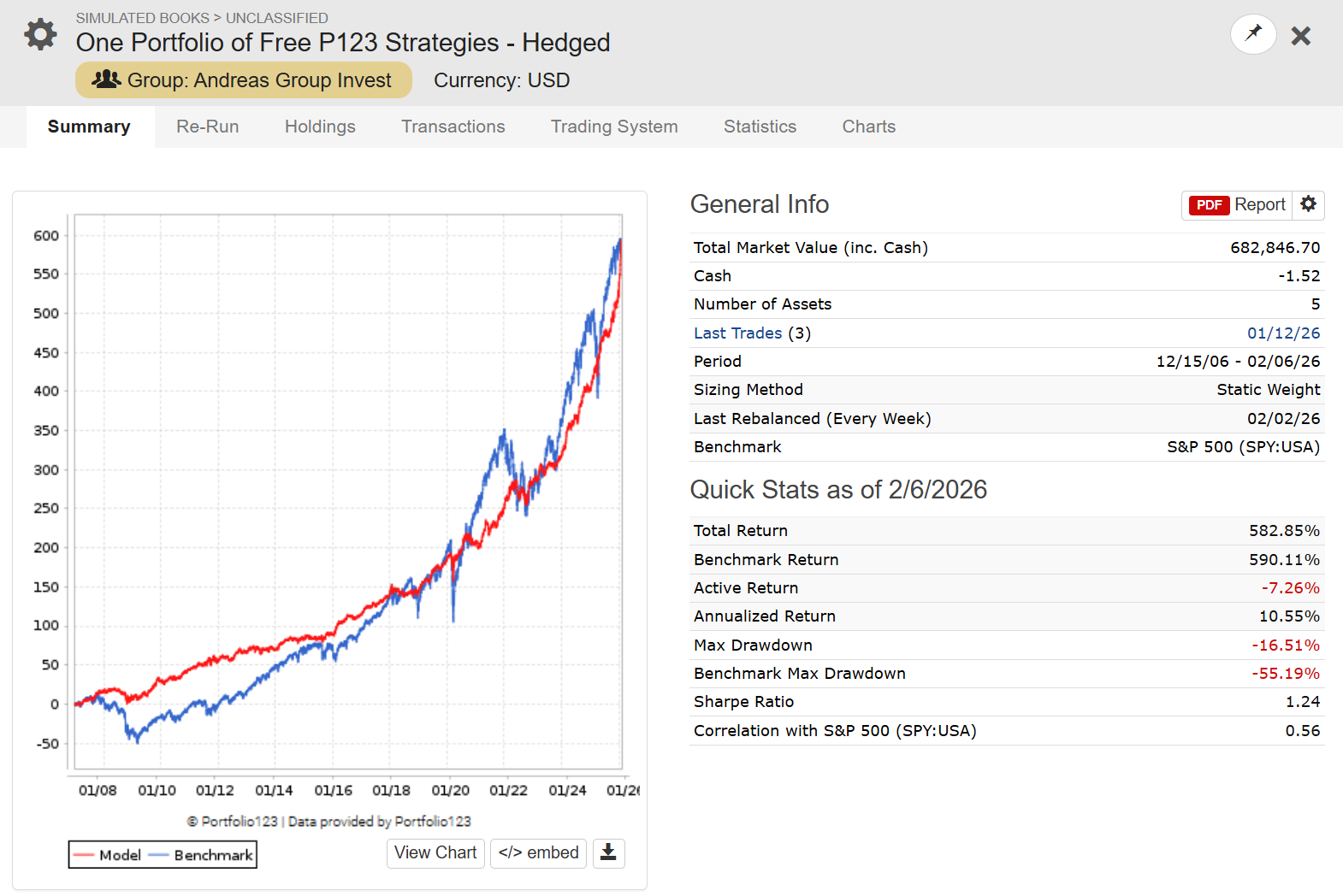

Yep, the strategy book also works hedged!

https://www.portfolio123.com/port_summary.jsp?portid=1854582

The Bottom Line

You don’t need to know which factor will work next.

You just need to own all of them —

and let mean reversion do the rest.

That’s Cross-Factor Mean Reversion.

That’s the book ;-)

Best Regards,

Andreas